3.7k words, 15 min read

Editor’s note: This is the 3rd of 5 essays in The Cycle, my series on healthcare’s revenue cycle. Ongoing writing to continue here.

Every few years, investors find a new market to draw lines through. Take something bundled — a platform, an industry vertical, a system that does too many things under one roof — and split it into specialized companies that each do one thing better. The term, “unbundling”, was coined in a 2010 post unbundling Craigslist (on a Tumblr, no less) - one ugly homepage full of loosely related categories, each a specialized startup waiting to be peeled off. Airbnb took housing, Indeed took jobs, dating apps took personals - and investors followed with billions in capital. The thesis got applied to Excel, LinkedIn, ChatGPT, every bundled incumbent investors could find. A useful mental model, or at least one that keeps the fundraising moving. Now it’s pointed at healthcare’s billing infrastructure.

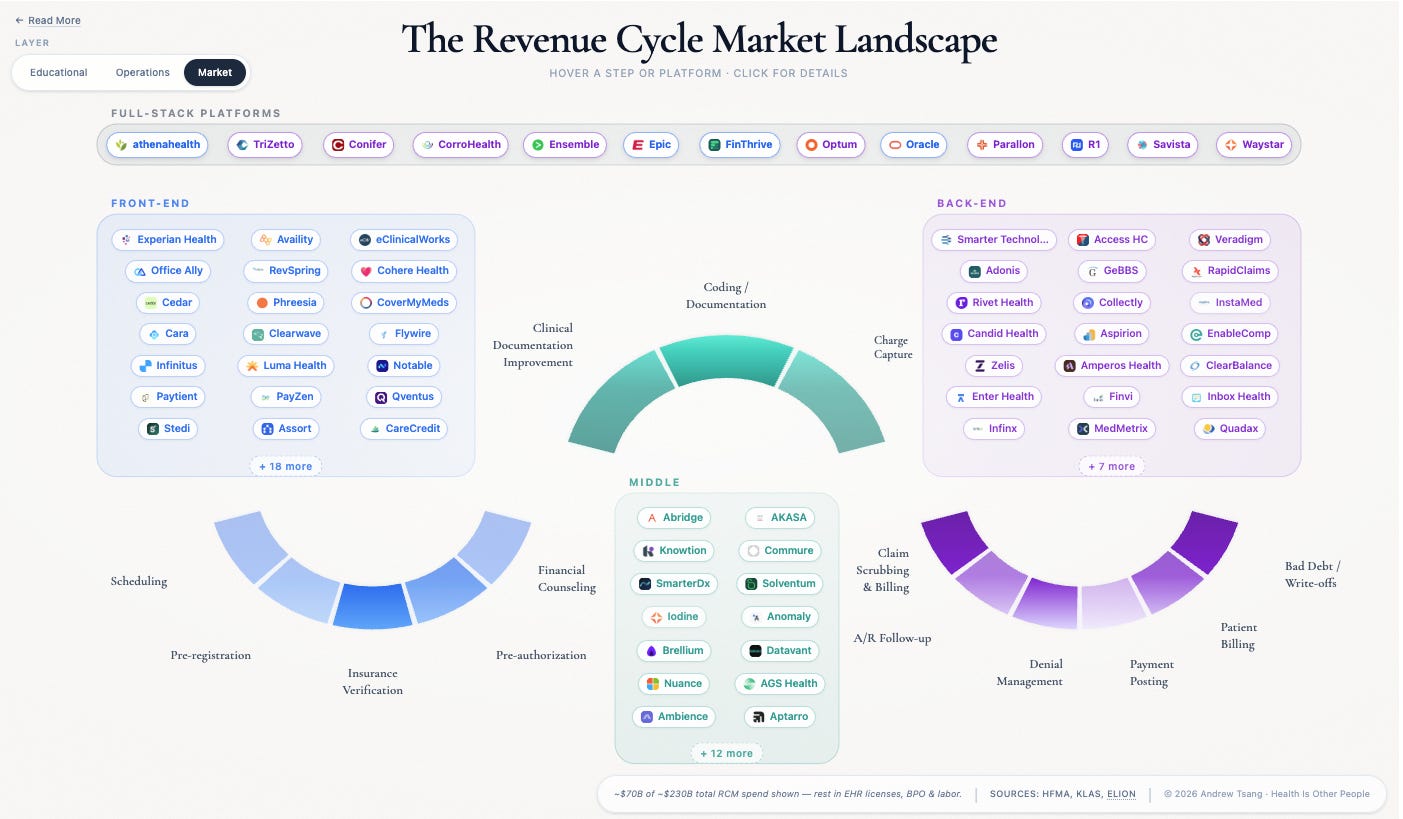

The administrative function that is the bizarrely-titled Revenue Cycle comprises roughly a baker’s dozen of steps from patient scheduling through final payment. Rev Cycle is a $300 billion industry ripe for unbundling - it is the admin layer between providers and payments worth roughly the GDP of Portugal. For investors, it looks like the perfect target: fragmented, software-underserved, exploding with AI potential. For providers, it looks like the opposite - another set of vendors competing for space on an already-crowded application stack, each one promising to own a piece of something that doesn’t work in pieces.

Market penetration varies across the arc. Cedar handles patient billing and collections. Waystar routes claims between hospitals and insurers. Solventum dominates medical coding — the translation of clinical documentation into billable charges. Cohere Health is building intelligent prior authorization — getting insurer sign-off before care is delivered. Each a specialist, each owning one piece of the arc. Exactly the shape the unbundling thesis looks for.

The biggest names in venture are bought in:

a16z - coined the healthcare unbundling frame. Their 2021 Akasa thesis: “For every $1 of revenue collected by a hospital, $0.25 is spent on the administrative tasks required to collect it.” Cedar at a $3.2B valuation, Akasa, and Commure all sit in the RCM portfolio.

Bessemer - State of Health AI 2026: 92% of health systems now deploying AI somewhere in revenue cycle.

Flare Capital (healthcare-specialist) - “Billions in Play” thesis: AI-enabled category leaders command a 30% valuation premium, station winners 5x. Portfolio: SmarterDx (crossed $100M ARR in 3 years before the New Mountain rollup), Cohere Health, Suki, Layer Health, Axuall.

Second Opinion / Scrub Capital - Christina Farr’s February 2026 “RCM Market Map” calls RCM “the first smash hit application for AI in healthcare.” Built with Bertelsmann Healthcare Investments ($200M U.S. health-tech fund with RCM as a named focus). Scrub Capital fund backs Elion - a procurement marketplace for hospitals shopping RCM vendors against each other. A meta-bet on the fragmentation itself.

If you’re a founder drawing a line on a market map in a Sand Hill Road conference room, you may walk out the door with a nice seed stage investment check.

But the same money funding the unbundling thesis is writing billion-dollar checks to bolt stations back together. The pitched exit is built, but the realized exit is bought. The market is mispricing one of them.

The Rollup Trade

The investor playbook for a vertical like revenue cycle is well-worn. Find a station where incumbents underperform, build the best point solution, win the wedge, and expand laterally. Unbundling is the playbook. What the pitch decks don’t say is that “expand laterally” is a euphemism for getting rolled up - acquired into a bigger platform spanning more of the arc. And rollups come with costs the market map doesn’t price: integration work, data model translation, change management across every hospital IT operation that adopts them. The playbook works for the founders and their VCs. Their exit isn’t an IPO - it’s the assembly itself, getting absorbed into a bigger platform. Getting bought is the realized thesis, even when it’s not the pitched one. The deck sells “build the category leader“ in something like denials management or clindoc, but the exit is being rolled up before the bilateral cascade catches the wedge. Both can be true at the founder level - but the durability case being sold to investors is doing different work than the liquidity case being executed.

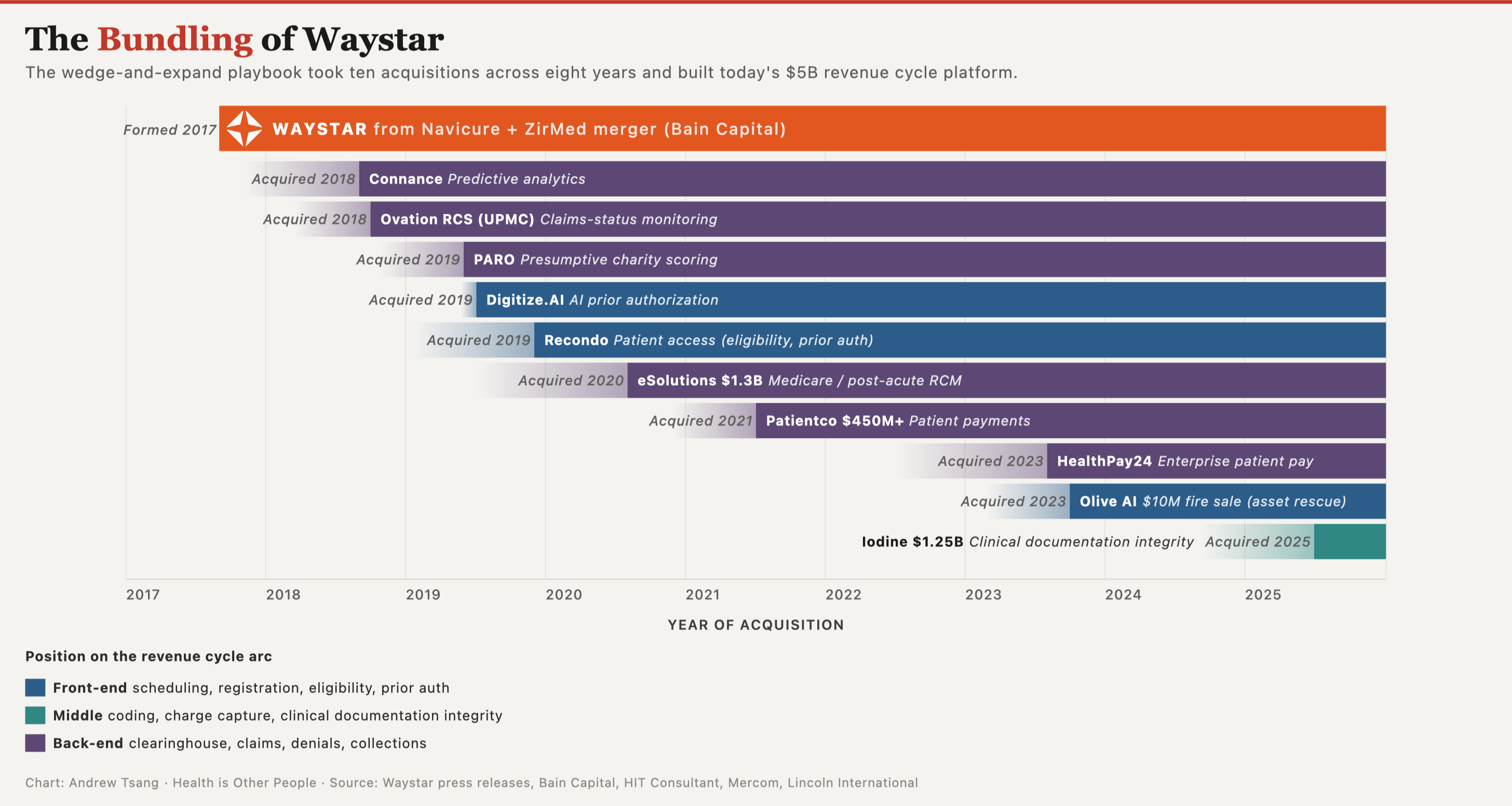

Waystar started as a clearinghouse - routing claims between hospitals and insurers, back-end plumbing. Since the Navicure–ZirMed merger formed the company under Bain Capital in 2017, they’ve made ten acquisitions across the arc:The Iodine deal in 2025 was the first time Waystar stepped upstream into mid-cycle clinical documentation - where the bill actually originates. The seven undisclosed deals between 2018 and 2023 were tuck-ins, almost certainly small. The three priced ones jumped from $450M (Patientco) to $1.3B (eSolutions) to $1.25B (Iodine). The cheap adjacent layers are gone - crossing into a new part of the arc now costs a billion.

Waystar isn’t a back-end vendor climbing a value chain. Three billion dollars of acquisitions across the arc is a company building to be the partner CFOs keep when budgets tighten - the moment specialists get cut in favor of vendors covering more of it.

Cedar ran the same play from the other end of the arc, moving upstream from patient billing into payer data, pre-visit workflows, Medicaid enrollment. Solventum, holding 75% of encoder installations in US hospitals, went the opposite direction - connecting coding downstream into denial prevention. Different starting stations, same move: when the problem you’re solving depends on the adjacent stations, you keep buying until you own them.

Having the best-of-breed point solution doesn’t really matter. The clearest evidence the market doesn’t reward quality is in KLAS ratings (which basically scores how much hospitals like their vendors) of end-to-end RCM outsourcers. Ensemble Health Partners at 95.1, best-in-class, but R1 RCM is at a meager 55.6. There’s a 40-point spread in ratings, but it doesn’t matter for market positioning. Both end-to-end solutions follow the same playbook, same access to durable contracts. R1’s customers just don’t rate them as highly. R1 is still public, still profitable, still acquiring because coverage of the revenue cycle wins the contracts whether staff like the product or not.

The same investors funding station-by-station specialists are writing billion-dollar checks to bundle stations back together. New Mountain Capital just rolled three companies into Smarter Technologies - $800 million in combined revenue, three stations bolted into one platform. Waystar spent $1.25 billion on Iodine for the same move. So, we can see unbundling doesn’t work as well here, but why?

The EHR Already Ate Half the Map

Let’s start with the landscape where these vendors compete. Investors draw 14 stations on the map, but the real game is narrower. Epic (and other EHRs) have already absorbed the front half of the arc; what remains is defined by what Epic can’t reach - the space between hospital and insurer, where every RCM startup plays and where most of them struggle.

When a hospital goes live on Epic, the front half of the arc comes built in - scheduling, registration, charge capture, the functions closest to the patient chart. The back half doesn’t - coding, clearinghouse, denial management, collections. An HFMA survey of 160 healthcare organizations shows the split as a gradient:

Functions closest to the EHR got absorbed first. Functions that grew up later, in the space between hospitals and insurers, stayed independent - because Epic can manage a patient’s chart, but it can’t manage the negotiation between the hospital and the insurance company over what that chart is worth. Everything remaining on the revenue cycle arc sits in that negotiation.

Third-party vendors live at the mercy of the healthcare economy. When hospitals bleed money, CFOs cut contracts - and that usually means consolidating onto Epic. They look at a vendor inventory with forty-something contracts, a dozen overlapping with something Epic already does, and a CIO pointing out that integration costs are eating the savings. I’ve run a dozen application rationalization projects (CIOs literally only want one thing) - if Epic has a tab for it, the standalone vendor contract will have a hard time getting renewed. This is not because Epic’s version is better, but rather because running two systems that do the same thing is expensive.

Here’s where the money concentrates:

Coding - $27B market, 51% third-party. Translating clinical documentation into billable codes requires payer-specific reimbursement rules the EHR doesn’t carry.

Clearinghouse - $14–17B, ~80% third-party. Someone has to route claims between systems that weren’t designed to talk to each other.

Denial management - $5–9B, 58% third-party. Payers and providers fight over every claim; the EHR can’t see the fight.

Every one of these markets exists because Epic can only see one side of the relationship.

Absorbed stations don’t disappear - they push the market upward. Epic absorbed scheduling (72% native), but the intelligence layer above scheduling didn’t get absorbed with it. Phreesia processes one in six US patient visits and grosses $500 million a year, growing 14-16% annually by owning the wrap-around layer Epic doesn’t bother to build - patient intake, eligibility, payment workflows. Epic took native scheduling. The money migrated to the layer above it.

Epic keeps moving the boundary. In November 2026, Epic Penny launches autonomous coding - an AI agent that turns clinical documentation into billable codes without a human coder in the loop. The same capability standalone AI-coding vendors built businesses around is now an Epic feature, bundled into the EHR contract. If Epic Penny works as advertised, the $27 billion coding market — the largest remaining independent station on the arc — starts becoming absorbed into the EHR. The attackable surface shrinks with every release.

What’s left to unbundle is what Epic can’t see: the stations that live in the space between hospitals and insurers.

Why the Unbundling Analogy Fails

In that remaining space, nothing stands alone. Revenue cycle stations are causally linked in ways Craigslist categories never were. You don’t need to buy a couch to find a date, and the dating section doesn’t affect people shopping for couches. But optimize coding and the patient’s bill goes up - higher-acuity codes mean bigger claims mean bigger coinsurance, a $1,600 patient responsibility becoming $2,200 on the same procedure. Optimize collections and patients defer future care. Every optimization at one station ripples through the others.

Even where categories actually are separable, unbundling underdelivered. “The Unbundling Fallacy” showed that many of Parker’s original Craigslist unbundlers failed because the bundled platform had network effects the verticals couldn’t replicate. “Excel Never Dies” made the case that Excel wasn’t unbundled either - the spreadsheet only got more dominant as SaaS tools proliferated around it. “The Rebundling of Craigslist” documented how vertical unbundlers hit structural limits. The same map got drawn for electronic medical records, and Epic grew market share while the unbundlers stalled.

If unbundling stumbles where the categories are loose, it cannot work where they’re chained together.

The Independent Market Is the Interdependent Market

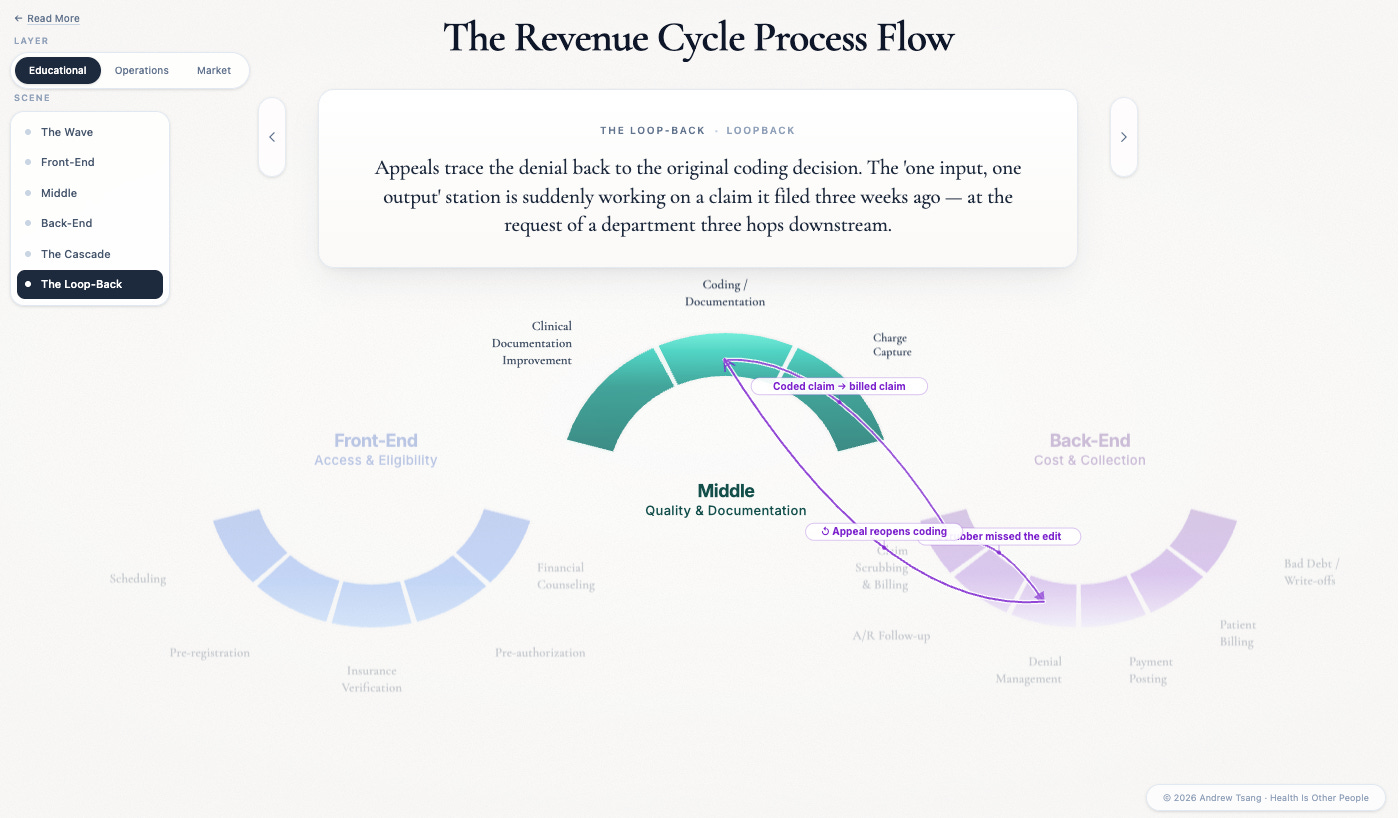

It’s not just that one station affects the next. In this remaining space, the stations feed each other in both directions:

Coding → sets up billing

Billing → sets up denials

Denials → trigger appeals

Appeals → reach back into the original coding documentation

And prior auth → gates the coding before it even happens

Every station’s output is another station’s input - and the loops run both ways.

These are actual experiences that revenue cycle teams face every month. Walk into a hospital revenue cycle office and watch one of those loops fire: the denial management team — the people fighting rejected claims — traces a rejection back to a coding decision, which traces back to a documentation gap, which traces back to a physician who didn’t know the payer changed its clinical criteria last quarter. The problem crosses four stations and three departments. The coding vendor has no idea the denial rate just spiked because of their optimization.

An investor betting on a coding wedge is betting on a station whose performance depends on what happens at denial management, three stations downstream, at a company they’ve never talked to. There is no wedge that gives you the next wedge. Each station is dependent on stations owned by someone else, which means the wedge-and-expand playbook can’t produce durability through organic growth. The only path to multi-station coverage runs through acquisition, which is why the durable companies in this market are the ones writing checks, not the ones building features.

The Curious Case of Olive AI

Olive AI is the case in point. Between 2018 and 2022, the company raised $900 million on a single-station wedge - automate prior authorization, win the wedge, expand laterally. Peak valuation hit $4 billion in 2021. By late 2023, Olive was wound down and sold for parts. The wedge didn’t hold.

I was *pinches fingers* this close to getting an Exec Director role at Olive in 2021. I made it to the final round, but didn’t make it by not having enough C-level client experience (probably fair) - which, looking back, told me something about what Olive valued. They were optimizing for executive relationships, not operational understanding of the systems they were automating. The public narrative about their collapse is about overpromised AI - brittle RPA, 27 pivots, five-fold headcount growth in eighteen months (all true). But the structural problem ran deeper. Olive tried to automate prior authorization as a standalone function. Prior authorization is a bilateral negotiation:

Hospital request → Insurer evaluation → (if denied) → Hospital appeal → Insurer re-evaluation → (loop until resolved or abandoned)

Automating one side of that exchange doesn’t work when the other side adapts. Olive built a faster fax machine for one side of the conversation.

After the collapse, Jeremy Friese — who’d run Olive’s payer market as president — bought the provider-side prior auth assets and founded Humata Health. The pitch he gave was an admission of error. Where Olive automated only the provider side of prior auth, Humata, in Friese’s words, would build “both sides of the fax machine” - the payer and the provider. He never says Olive got the architecture wrong. The product rebuild says it for him: you can’t win a station in this market from one side of the negotiation. Even the founders who watched it fail had to come back to sit on both sides of the fight.

There’s one type of station that escapes this trap: coding. Nym, Fathom, and CodaMetrix turn clinical documentation into billing codes - one input, one output, one buyer per hospital, clean boundaries. They’ve built standalone businesses because the transaction is one-directional. Every other remaining station is bilateral. The vendor sits between hospital and insurer, mediating a fight neither side can resolve. That’s why the bilateral stations get rolled up: no one can run them alone.

The Friction Market

Revenue cycle is the billing apparatus of a permanent disagreement. Hospitals and insurers don’t agree on what care is worth, and revenue cycle is the system that processes the disagreement.

The money that analysts size as “the revenue cycle market” is the cost of processing claims through a permanent, adversarial negotiation between hospitals and insurers. Every station exists because the two sides can’t agree:

Coding translates the hospital’s documentation into the insurer’s reimbursement language.

Denial management processes the insurer’s no’s against the hospital’s yes’s.

Prior auth is where the insurer gets to veto care before the hospital delivers it - the only stage in the cycle where the negotiation runs before the service exists. The earlier the fight, the more leverage the insurer has.

Clearinghouse routes claims between hospital systems and payer systems that were never designed to talk to each other. It translates data formats and routing rules every time a claim moves between the two parties - the plumbing that exists because the two sides can’t agree on shared data standards either.

Collections picks up whatever balance the hospital-insurer negotiation didn’t resolve. When the two sides stalemate, the unpaid portion gets shifted to the patient - the only party in the chain without leverage to fight back.

Each is a tollbooth on the disagreement. The bigger the disagreement, the bigger the tollbooth.

Every vendor in this market is a middleman in that fight. And every optimization — faster coding, smarter denials, automated prior auth — entrenches the fight rather than resolving it. The vendors build rails so dependent on the current terms of the hospital-insurer relationship that they harden the very dynamics they claim to streamline. Cedar’s 2026 Trends in Patient Payments report says it plainly: patients are “the one payer class where providers can still influence outcomes.” When the bilateral fight reaches stalemate, the costs get pushed to the one party that can’t fight back.

The arms race confirms it:

Denial rates climbed from 10.15% to 11.8% between 2020 and 2024

Medicare Advantage prior-auth appeal overturn rates run above 80% - most appealed denials in MA are wrong on the merits

Volume keeps rising anyway, because the fight is the point, not the accuracy

Both sides spend billions on automation to maintain the same relative position. The vendors are the only clear winners. They bill for every appealed claim, every re-submitted authorization, every dispute that never resolves. Friction itself is the product.

Revenue cycle is too interconnected to unbundle and too sprawling to consolidate. The market exists because of the relationship, not despite it.

Every company operating in this space is optimizing within the current terms of that relationship - and those terms are themselves being rewritten:

Prior auth is getting a clock on it. The CMS-0057-F mandate takes effect January 2027 - payers have to use FHIR APIs and respond within 72 hours (7 days for urgent). The front-end of the fight just got compressed from a month to days. Every vendor selling prior-auth automation gets a moving target.

The collections lever just disappeared. The Consumer Financial Protection Bureau’s January 2025 rule bars medical debt from credit reports - providers lose the threat that made patients pay. Cost pressure routes back upstream to the hospital, which routes it back into the rest of the cycle.

States are picking surprise billing apart one industry at a time. Beyond the federal No Surprises Act, state legislatures are adding rules on ground ambulances, behavioral health, air ambulance pricing, and out-of-network disputes. Every statute moves the line on who eats the loss when the fight ends in stalemate.

This is the ground under every vendor’s feet, moving faster than any of their product roadmaps.

After COVID, I briefed Chuck Christian, CTO at Franciscan Health, on an IT application rationalization (basically, which IT vendor contracts to keep, which to cut). With nearly 40 years of IT experience, he told me the ebbs and flows of the market: best-of-breed point solutions wins for a stretch, then something breaks in the economy and buyers pull everything back under one roof for rationalization. Then the market loosens with new innovations, and the point solutions get back in. But ultimately, the issue wasn’t which tech was best: it was who’s a partner and who’s a vendor - which of these companies will still be here in ten years, when the tech is woven through operations and I can’t rip it out?

This is how institutions think about durability of vendors. A startup’s Series B runway rarely overlaps with a hospital’s implementation timeline. The hospital has twenty specialists to pick from, and most of them won’t survive the next wave. Which means the premiums Flare Capital cited at the top — 30% extra for AI-enabled vendors, 5x for the station winner — aren’t being paid because investors think the company will last. They’re being paid because investors think someone else will buy it. That’s why IPOs happen a lot less in healthtech - the usual outcome is rollup.

The payer-provider fight is structurally dysfunctional, and that dysfunction rewards positioning over performance. CFOs trimming IT budgets pick the partner who covers enough of the arc to be worth keeping, regardless of how staff feels about the product. The worse the underlying market gets, the more valuable broad coverage becomes. Point solutions in this market end up as components in someone else’s stack. The fight stays broken; the broad-coverage vendor stays paid. The moat compounds across cycles, not quarters.

And the fight is what scales. Fix one station and the next one breaks. AI just makes both sides faster - sharper denials meet sharper appeals, prior-auth bots meet payer counter-bots. The market grows because the fight grows.

Which is the thing that should change how this asset class is priced. The $300 billion isn’t the size of the RCM software market. It’s the price the system pays to keep the disagreement going. Investors are pricing it like software. It’s friction - and the durable companies are the ones building for the fight, not its end.

This piece extends a thread running through Not a Cycle and Cycles and Triangles. Coming next: how policy is rewriting the terms underneath, and what survives when the bundle finally breaks. - A.T.

Nothing here is investment advice. The companies named are illustrative of a market dynamic, not recommendations. I hold no positions in any of them and have no current consulting engagement with any company named.

The companies named throughout this piece are representative, not exhaustive - Stedi’s January 2026 map catalogs 500+ vendors across the arc, Second Opinion / BHI draws another version, and no two agree on where the lines run. Which is its own evidence for the argument above.

Excellent piece! Perfectly articulated : "The $300 billion isn’t the size of the RCM software market. It’s the price the system pays to keep the disagreement going"

Excellent work on this one 👏