6.8k words, 27 min read

Editor’s note: This is the 4th of 5 essays in The Cycle, my series on healthcare’s revenue cycle. Ongoing writing to continue here.

Consider the claim: two charges in one word. A chronicle (the record of the care, what was done to you and why) and a contention (the provider’s sworn assertion that a sum is owed for it). One document that tells the story of your care and opens the argument over its price. Captured, coded, checked, charged, and then, challenged - and a contested claim gets caught in a cycle.

Healthcare finance moves $5.3 trillion a year, most of it as a claim - and a claim is a bill in dispute before it is ever paid. It somehow runs on backwards economic logic: the care first, the price last, the payer keeping the right to dispute the bill after the fact (whoops - wrong code, not medically necessary, out of network). One of my idols, the legendary Princeton economist Uwe Reinhardt, distilled the whole problem down to “It’s the prices, stupid”... but what is often overlooked is that a price has to be agreed, and what healthcare agrees on is the rates - while what is owed is asserted and answered, claim by claim. A credit-card swipe is consent before the fact - a claim is a trial after it.

The initial instinct, always, is to regulate the reimbursement - though not to set the price itself (the anti-capitalist sin American politics won’t commit, leaving the price to the market) - so the rules pile up around it: standards, disclosures, deadlines, courts, each promising to bring the two sides to agreement. And this is how a country came to settle the economics of its largest industrial market through a claim - one contest at a time.

A trial, not a transfer

Nowhere else does moving money require a trial at all. In 2025 the Federal Reserve’s Fedwire system moved $1.15 QUADrillion (a number so incomprehensible I think I’ve typed “quadrillion” twice in my life, including that one) and adjudicated not one of those transfers. The securities clearinghouses settled 3x more than that; the network behind every payroll and direct deposit moved $93 trillion more.1 Sums that dwarf all of American medicine, cleared fast and clean, because every one of those rails has the one thing healthcare does not: a price agreed before the money moved.

Healthcare runs the opposite of other financial infrastructure. A disputed card charge is rare enough that the card networks punish a merchant who lets it cross a fraction of a percent; the automated network caps unauthorized returns at 0.5%; even stock trades fail to settle only 2-3% of the time.1 In healthcare, ACA marketplace insurers denied nearly 20% of in-network claims in 2023 — 86 million denials, of which patients appealed less than 1%. Everywhere else, a disputed payment is the exception; in healthcare, it is the whole job of the revenue cycle.

Insurance looks like the exception - it too pays after the fact and argues constantly. But other insurance fixes its price at underwriting, and even its payout fights (the adjuster’s estimate against the body shop’s) settle against a market that exists outside the policy — the going rate for a fender, a roof, an hour of a contractor’s time. Healthcare fixes only the rates, so it fights on two fronts — whether the care was warranted and what it was worth — with no outside market to referee either one. Other insurance argues the event; healthcare argues the event and the bill.

Everything but what’s owed

Govern a transaction and you reach for the same few tools: a standard (both sides bill in one language), disclosure (the terms sit in the open), a clock (the answer comes in time), and when those fail, a court to settle what is left. Beneath them all should sit one more — an agreement on what is owed, struck before the money moves — and the straight road to that one runs through the cardinal sin of a market economy: setting the price.

Whatever you think of the sin (set the price, so the argument goes, and the money for the next drug dries up), American health policy has kept the commandment.2 So it standardizes the codes, posts the prices, puts the gate on a clock, even builds the court for disputes - everything but settle what is owed. The rates themselves were settled all along (commercial insurers negotiate them into contracts before any patient walks in; Medicare just posts its own). But a rate only names the number; whether it is owed is what every claim re-opens.

What is owed stays unsettled for a plain reason: the country has hated every fix more than it hates the fight. And each rule arrived with a forecast attached — the savings it would book, the behavior it would change — and the forecasts are worth keeping score on as we go: where a prediction breaks, and which way it falls, both point to what the rule actually did.

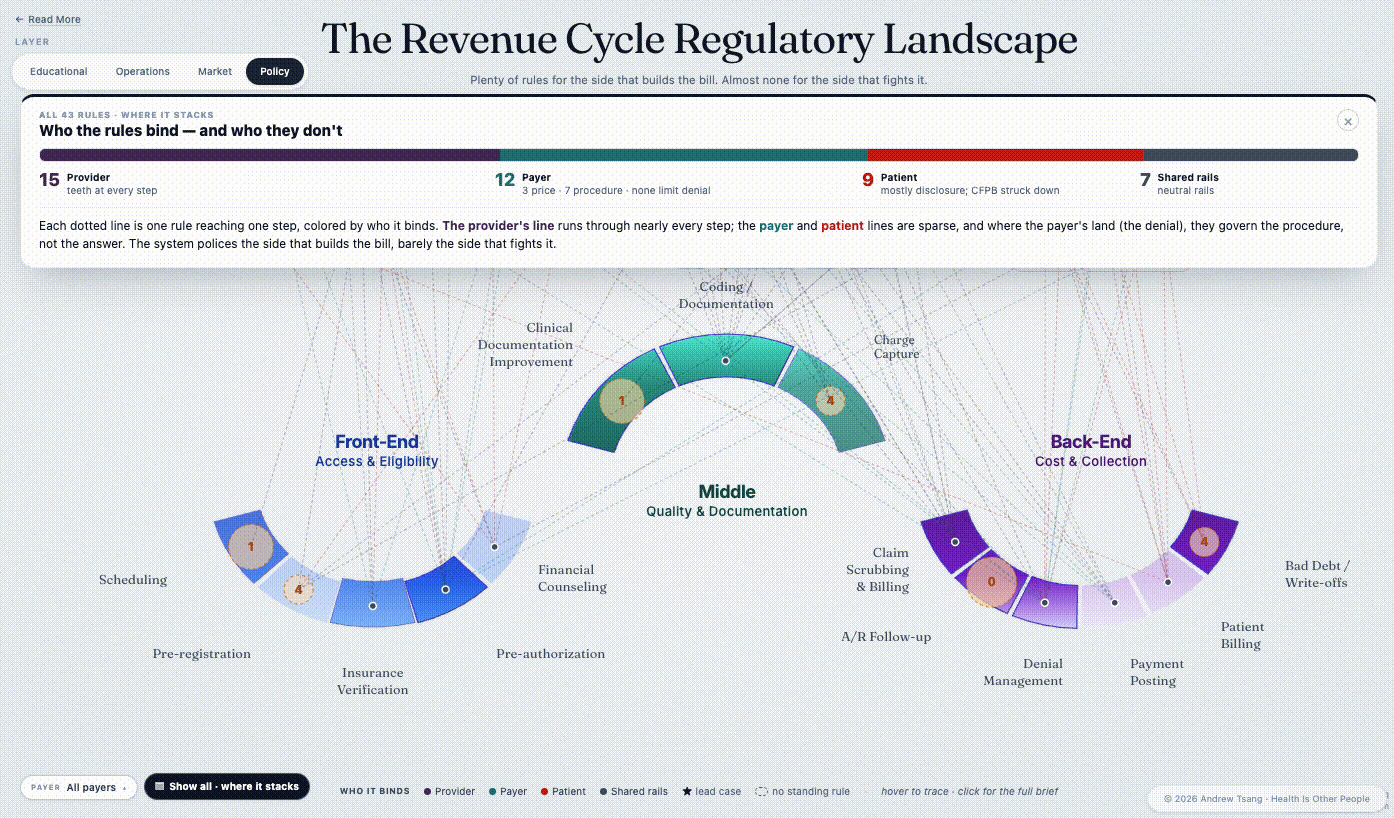

The map below sets every rule in this essay against the fourteen stations of the cycle - where each one lands, and the gap at the center where none of them do. (It’s interactive - open the live version.)

Start with the one that sounds easiest: the standard - the rule that fixes what a claim is even allowed to say.

A shared language

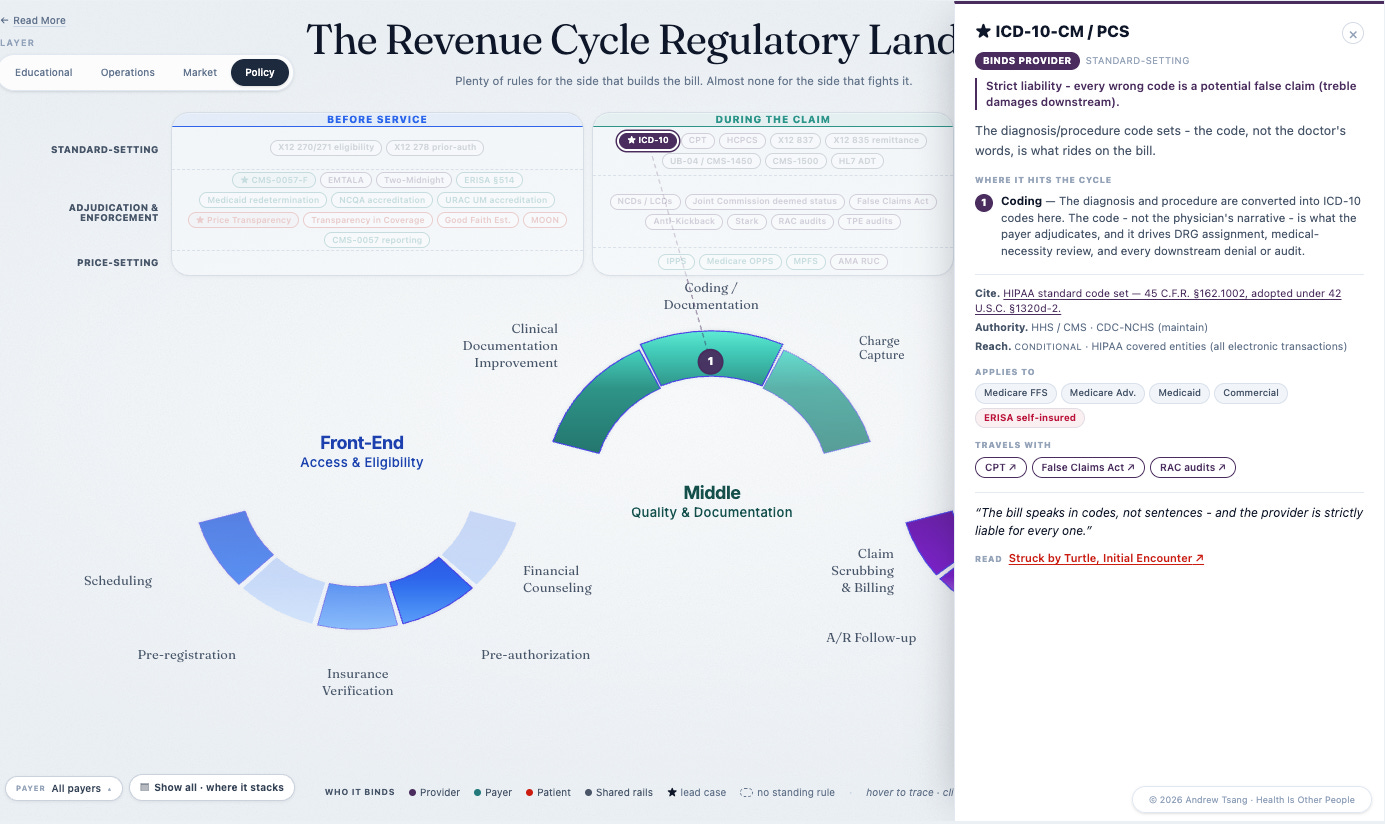

A standard sets a shared language - the clearest way to get two parties to reach an agreement. In the revenue cycle that language is codes; nothing can be priced until it has one. When a diagnosis, a procedure, a supply each resolve to one standard code that means the same thing on both sides of the bill, the claim can settle almost without a human - the payer reads what the provider wrote, and the two numbers match. That is the whole promise: a standard turns a negotiation into a lookup. It is also the first thing anyone reaches for when the cycle feels like chaos - just standardize it.

And the cycle already runs on a stack of them: ICD for the diagnosis, CPT and HCPCS for what was done, the X12 837 the claim rides on, the UB-04 behind it. All of them converge at coding, the station where someone reads the clinician’s chart and translates the care, line by line, into the codes a claim is built from. And coding is where the biggest code-set change in the industry’s history landed: the roll-out of ICD-10.

Early in my healthcare career, ICD-10 was finally changing over — one narrow technical swap, mandated by HHS under HIPAA’s authority to pick the industry’s code sets — and it still took America a decade of false starts: the go-live slipped, then slipped again when Congress kicked it another year inside a Medicare bill. I was a young consultant at Deloitte then, and one of the services we were pushing was change management for ICD-10. The rest of the world had been running on ICD-10 for some two decades; why wouldn’t we adopt it too?3 When the switch finally landed, on October 1, 2015, the working vocabulary of American diagnosis went from roughly 14,000 codes to 68,000. The trade press had spent two years predicting catastrophe.

Every forecast pointed the same way. The American Medical Association called the switch a “crushing burden,” citing a study that put small-practice conversion as high as $226,000; the trade press warned of coders seizing up, one claim in five rejected, billions in cost industry-wide. But the complaints came too early to be about the workload: providers were calling the standard unfair before a single new code had been filed. They weren’t really fighting the vocabulary; they were fighting the scrutiny - every new code was one more thing a payer could question.

None of the predictions came to pass. Denials held flat - the Medicare rejection rate came in at 9.9%, a hair under its pre-switch baseline - and a 2018 analysis put the real small-practice cost near $1,200, not the hundreds of thousands the AMA had forecast. Modern Healthcare’s verdict on go-live day: “like Y2K, so far.” (The one claim in five did arrive eventually - ACA marketplace insurers deny about that share today - just in a different market, a decade on, with no code switch to blame.)

But a standard is supposed to take friction out - one language, fewer things to argue about. ICD-10 put friction in. Sixty-eight thousand codes meant more to specify, more to document, and more to dispute - every new distinction is one more thing a payer can deny and a provider must defend. An entire documentation industry grew up to work the new specs - a $4.5B market by 2023. And it cut both ways. When the HHS Inspector General audited 200 severe-malnutrition claims, 173 were billed wrong: nearly $1B in overpayments from a single family of codes. So the predicted catastrophe never arrived - but the miss is only half the story.

None of that was in the forecast. The decade’s real product was a new layer of dispute, billions of dollars of it, grown on a rule everyone had filed away as a non-event. The standard was meant to help two sides agree; instead it gave the disagreement more places to live. The providers turned out right, just not for the reason they gave: the catastrophe they predicted never came, but a quieter cost did - the vendors, the documentation industry, the audit machinery, the AI that now codes against the AI that now denies, all of it sitting on top of the transaction. HHS adopted a code set; everything else grew up around it, beyond the forecast and beyond the rule. Over a decade later, that added layer is the ground every later case stands on.

It all lands at one station: coding, where the chart becomes a billable claim. That is where ICD-10 hit hardest, and where the machinery it spun off now sits:

Cards on the table

A shared vocabulary had not settled the fight, so the next mandate went at the price itself - and where ICD-10’s forecast had been all doom, this one was all promise. Post the prices, the thinking went, and the patient could finally see the cards the house had always kept hidden - and play a hand of her own.

The cards did get turned over: the Hospital Price Transparency rule made hospitals post their payer-specific negotiated rates in 2021, and the Transparency in Coverage rule made the insurers post theirs in 2022. The system guards one number above all the rest: what this payer actually pays this hospital for this procedure - the rate written into their contract, the number every bill is measured against. That number became law to disclose, twice over. Both rules chose the same vehicle - the machine-readable file, a giant structured data dump built for computers rather than people, on the theory that someone would build the people-friendly layer on top.

I watched clients comply with Transparency in Coverage (pronounced “tic” in meetings), and just publishing the rates the rule demanded became a months-long technical and operational lift inside the plans, the kind that pulls people off everything else.4 And what the mandate mostly bought was the files themselves - machine-readable, and aptly so (you would need a fairly expensive machine to read one). Single files ran toward a terabyte, formatted so that neither a patient nor most payers could open them, let alone compare what was inside. Hospitals had the same problem, only sharper: a community hospital has no transparency team to spin up, and the smallest independents post genuinely good data but can’t get the file format right. The files went up; the prices inside them never moved.

And the game didn’t stop. Commercial prices kept right on climbing - by 2022 RAND put the average commercial rate at 254% of Medicare, up from 224% two years before. Disclosure didn’t pull prices down; it handed the underpaid hospital a target. The one earning less than its crosstown rival could now see exactly how much less, and exactly what to ask for at the next negotiation. Where rates moved together at all, they moved up, because a posted rate is a target. The most favorable evidence makes the same point: a study of cancer prices found that posting the files moved nothing on its own, and prices dropped only where hospitals went further and posted rates a person could actually read, service by service - and even then slowly, in the most shoppable corner of medicine. The patient never became the player the rule imagined, either. The people working the files are employers, vendors, and researchers - not patients.

Price disclosure was never going to end the contest anyway, and weak compliance isn’t the reason - 7 in 10 hospitals now meet every requirement. The trouble is that posting hasn’t changed behavior, because neither side wants the rule to work. The hospital does not want its discounts shopped, the insurer does not want its rates undercut, and both already knew the numbers, because both negotiated them. Even full compliance just hands each side better ammunition for the next round of contracts. Seeing the other player’s hand makes for a fairer game, not a shorter one. The next mandate would come at it the other way - a hard deadline instead of disclosure - and still reach only half the system.

The permission slip

If you have ever waited days for an insurer to approve a scan your doctor already ordered, you have met prior authorization: the permission slip the payer demands before it will pay — the one check that comes ahead of the care. Prior auth may be the most hated process in American medicine - patients hate the wait, doctors hate the paperwork, and the plans defend it the way you defend a dam: not out of love, but for fear of what floods through without it. In 2024 the government finally moved - it set out, on purpose, to fix a piece of the cycle. The rule (CMS-0057-F, a number you are not meant to remember, but one that keeps a whole industry on edge) put the insurer on a clock: seven days to answer a routine request, seventy-two hours for an urgent one, electronic pipes by 2027, public reporting on how often it says yes, and $15 billion in projected savings over a decade.

But the clock is all it governs. The rule sets how fast the insurer must answer - not what the answer can be. A “faster no” is still a no, and the denial rate doesn’t move. It speeds the payer’s response without touching the patient’s outcome. Compare the pace: a card authorization clears in a second and commits the money; a prior auth can take a week and commits the insurer to nothing - the scan it approves today can still be denied when the claim arrives. Part of the week, to be fair, is real work. Behind many prior auths sits an actual clinical review — a nurse reading the chart, a medical director, sometimes a peer-to-peer call with the ordering doctor — and the plans do not have the clinicians to keep pace with specialty demand. That is the trap in the deadline: you cannot hire your way to seventy-two hours.

And it reaches only half the people it is for. Whether the rule covers your care depends on a line on your insurance card you have probably never read: if your coverage runs through a self-funded employer plan — about two-thirds of workers with employer coverage — then ERISA (a 1974 pension law with nothing to say about scans) puts you outside the rule entirely. On that side of the line the employer designs the benefit and a third-party administrator runs the denials under whatever the plan documents allow - a prior auth that can take as long as the plan likes, a denial that can arrive after the care, the terms written into a benefits booklet only the employer signs. The same scan gets the same denial, but with two different rulebooks - the dividing line set by a law written before the problem existed. A rule that governs half a market is one the market can afford to wait out.

So the deadline lands on a process that was already out of staff, and the way out is software: payers are buying it. Authorization requests that took a nurse a week come back from an algorithm in seconds - approvals instantly, denials instantly, the clinical review compressed into a model neither side trusts. This case is still unfolding as I write: the deadlines hit in 2027, the $15 billion is still a projection, statehouses keep passing their own versions.5 But it is the same miss again - the rule written to tame prior auth is automating it instead. The week-long wait becomes a same-day no, and the person you argue with about it stops being a person.

A room to fight in

Standards, disclosure, a clock - every rule so far had left the two sides to fight it out between themselves. This time the government went further. By the late 2010s the surprise out-of-network bill had become a national scandal — the anesthesiologist you met only on the bill, the ambulance that was somehow out of network — and the anger crossed every line that usually divides healthcare politics: patients, doctors, employers, both parties in Congress. When two sides cannot agree on a price, the oldest answer in the book is a neutral third party - it is how divorces settle and how labor disputes end - and healthcare’s fundamental disagreement looked like exactly the kind of fight you hand to a referee.

So the No Surprises Act barred those doctors from billing patients and sent the leftover fight to arbitration. Each side names a price, an outside arbitrator picks one, no appeal. The patient steps out of the crossfire, and the payer and the provider argue it out in a back room at the end of the cycle - the provider wanting more, the payer wanting less. On its own terms it worked: patients stopped getting ambushed, and it should have kept working. What the law had built, though, was a private courtroom for the most contested transaction in American medicine - and word got around.

The government anticipated about 17,000 disputes a year; doctors brought 1,200,000 in the first half of 2025 alone, and won roughly 88% of them. A whole industry grew up to feed the machine - firms that exist only to file arbitration claims by the thousand, radiology groups with a hundred and fifty people doing nothing else. The arbitrators did well too: paid by the case, they collected $885 million in three years, and something predictable happens when the referee is paid per fight and prefers one of the fighters. As one health economist put it to the Times: “Arbitrators are people, and the typical person likes physicians.” The insurer walks in with baggage - owing, in every hearing, for every denial it has ever issued - and the doctor walks in as the one who saved a life. Not that every doctor in the queue saved a life: one Manhattan plastic surgeon (who owns the trademark Dr. Penis) has filed six thousand claims through the system and won better than 85% of them.6

You can see where the No Surprises Act hits: billing and AR follow-up, where the out-of-network claim gets fought out long after the patient has gone home:

The people who built it can see it. The congressman who wrote the law is glad it passed and says the arbitration needs reining in; an insurance chair calls it a recipe for higher costs with no checks, no balances, no oversight; the plans have sued by the dozen, and judges keep throwing the suits out, ruling that Congress never meant for courts to second-guess the arbitrator. So the awards stand, premiums rise to cover them, and the fight grinds on inside the room built to end it. Refereeing the fight is the most the US government has ever done about the American medical price - and it leaned on a naive hope that, handed a referee, the two sides would finally settle. The forecast completely whiffed (seriously, only 17k disputes annually?). Even by the standards of policy misses this one was extreme, and it broke one way — toward the providers, who took advantage the moment the doors opened.

Where the rules run out

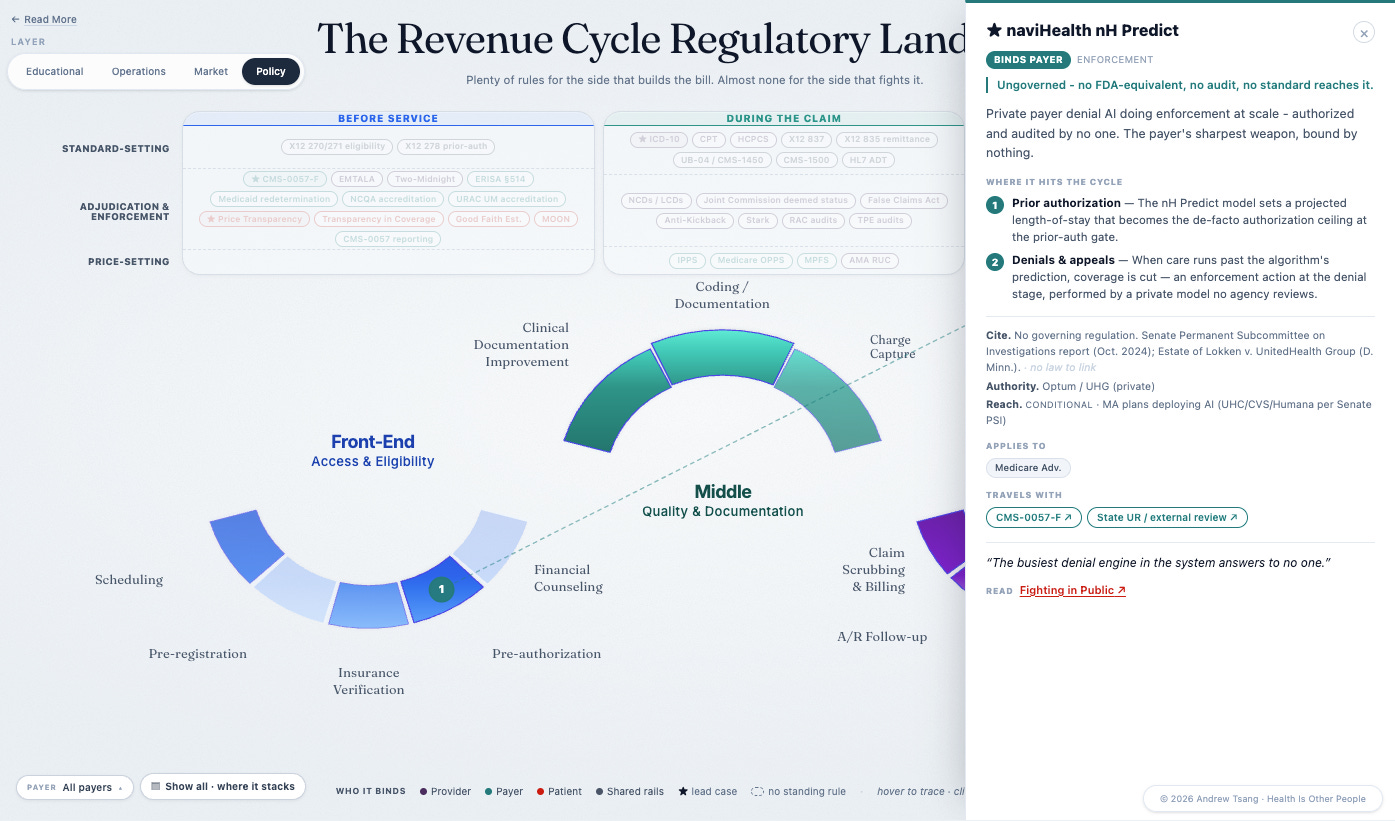

Every case so far has been a rule that came up short: a standard that bred more to fight over, a disclosure that moved no price, a clock that only speeds the denial, a court that drowned in its own filings. Failure on that scale tempts an obvious conclusion — stop writing rules and let the market sort it out. naviHealth is what the market sorting it out looks like: one side stops waiting for a rule and settles the fight itself.

The soft part of the revenue cycle is recovery — the weeks in a rehab unit or a skilled-nursing bed after the hospital lets you go, where someone has to decide how many more days the plan will pay for. It is a real judgment, and for years no rule watched it closely. So UnitedHealth bought the judgment: in 2020 it acquired naviHealth, a post-acute-care company, and ran its nH Predict algorithm inside the largest Medicare Advantage plan in the country — software that looked at a patient and forecast, almost to the day, how long recovery should take.

The machinery inside a payer runs out of sight - not hidden exactly, just unwatched - and it stays that way until the public finds out. The finding-out, this time, was the work of Casey Ross and Bob Herman at STAT — two years of reporting, internal documents, former employees on the record (the closest thing this industry has had to its own Spotlight team). In March 2023 they published “Denied by AI“ — a Pulitzer finalist, and the reason any of this is on the record at all. The nH Predict forecast how long a patient should need; UnitedHealth then pressed its own nurses and case managers to keep their decisions within 1% of the forecast. A tool meant to advise had become a quota in everything but name, and staff who pushed back were overruled. The story opened on an eighty-five-year-old woman with a shattered shoulder whom the algorithm had given 16.6 days; on day 17, her plan stopped paying. I bet every insurer in the country was shitting their pants wondering if their own operations were doing the same.

Once it was on the record, the numbers came. The Senate Permanent Subcommittee on Investigations pried loose UnitedHealth’s internal data: post-acute denials up from 8.7% in 2019 to 22.7% in 2022, skilled-nursing denials from 1.4% to 12.6%, a ninefold jump in denial rate. The AHA put Medicare Advantage denials up 55.7% from 2022 to 2023. Inside that data, in 2022 alone, were some 34,000 skilled-nursing denials. One of them was a 91-year-old man named Gene Lokken.

In May 2022, Lokken fell and fractured his leg and ankle, then spent a month in a SNF just healing enough to be cleared for physical therapy. His therapists charted slow, real progress; UnitedHealth paid for 19 days of it, then declared him safe to go home. The algorithm said his recovery was finished. His family looked at a man who still could not walk and disagreed - and kept the therapy going with about $150,000 of their own money over the year that followed, until he died in July 2023. That November his estate sued, and the complaint put it in writing: when patients appealed these algorithmic cutoffs, roughly 90% were reversed — a model wrong nine times in ten, ending tens of thousands of recoveries, counting on how few families would fight. The Lokken estate’s suit has drawn a fraction of the exposé’s press, and it is the sharper instrument: a family asking a court, in plain terms, whether a payer may hand the end of someone’s care to a forecast.

And you can see where these denials cluster: the coverage reviews and denials deep in recovery, the stretch of the cycle no rule reached:

The patient caught in the middle of all this machinery is in week three of a recovery the software has already closed out. Strip the fight down and this is the contested transaction at its rawest. In the rest of the economy, two sides agree on a price before the money moves; here the payer decided, on its own, how much more recovery it would pay for — none — and had the software to make that decision stick across tens of thousands of patients at once. Providers armed back, and the arms race now runs both ways: providers running AI scribes to push their diagnoses up, payers running automation to knock the claims down, Cigna switching on software in October 2025 that automatically downgrades its priciest claims. Underneath the machinery it is the same yes and no the two sides have always traded - automated now, and sounding more official for it. Washington has noticed, and done little: Senator Warren and others pressed CMS for guidance; the agency gestured at the problem and took no power to audit or certify. No federal vehicle, as of this writing, governs the algorithms a payer uses to deny.

It took that lawsuit, because the courts were the last door standing. In February 2025 a Minnesota court threw out the healthcare claims — bad faith, deceptive practices — as preempted by the Medicare Act, and let stand only the contract claims (the breach, and the good faith implied in any contract) — the law that governs a broken fence or an unpaid invoice. The one body that could touch naviHealth could reach it only as a contract dispute - and a suit brought by a dead man’s family is doing the work no regulator did. The case is still moving through the court as of this writing.

So the market sorted it out. One side got a model, the other side got a lawsuit, and the patient in the middle had a say in neither - his family just got the bill. The rules in this essay are inadequate; the stretch with no rules was worse. Imperfect referees still beat an empty field.

The floor

The word has been confessing it all along. Claim comes from the Latin clamare, “to cry out” - the root it shares with clamor, exclaim, proclaim, counterclaim. English took it up in the thirteenth century as a “cry for what one is owed”, and the meaning has held ever since: you claim what someone might withhold. A bill expects payment; a claim expects an argument - the word assumes an audience that can say no. The industry’s own name for its invoice concedes the fight, and every rule so far took the concession at face value: a standard for wording the cry, sunlight on its going rates, a clock on the answer, a courtroom for when the answer is no.

Look back across the regulatory map and the patchwork is plain. The five cases here were drawn from dozens - I lost count past forty, most of them code sets and transaction formats no reader would tell apart (the 276 from the 277). And every one of those rules lands somewhere around the claim - never on the one thing at its core: what is actually owed.

(It’s interactive too - explore the field on Datawrapper.)

Rule after rule, station by station, written for parties that could hardly be less alike -health systems with compliance departments the size of agencies, small hospitals drowning in the same requirements, a thousand-plus payers of every capability, and the patient billed for the friction among them. Which raises the obvious question: why isn’t there just one law that covers the whole revenue cycle?

There was an attempt - and you already know its name. HIPAA, the Health Insurance Portability and Accountability Act, is the most famous statute in American healthcare, mostly for things it did not originally contain (the privacy rules everyone associates with it came years later, by regulation). What Congress actually passed in 1996, by lopsided bipartisan margins, was a bill about insurance: letting workers carry coverage between jobs, limiting preexisting-condition exclusions. The part that matters to this essay rode along almost unnoticed — a title called administrative simplification, added on the theory that if the whole industry billed in one electronic language, the paperwork would stop eating medicine. A floor under every station, rather than one more rule dropped on top - laid in a world of paper claims and fax machines, by people who could not have pictured an algorithm denying a nursing-home day.

Read the name again, because it gives the game away. Insurance, Portability, Accountability... the moving of coverage, the accounting of the transaction, and nowhere in it health, or care, or a patient. A road is built for the traveler; this one was built for the transaction.

HIPAA’s administrative-simplification provisions were meant to do for the cycle what road signs do for a highway: give everyone one language. They standardized the electronic form a claim rides on and the form the payment comes back on, locked the diagnosis and procedure code sets in place, and handed every provider one number the whole system would recognize. It was federal, it was ambitious, and it worked - the rails it laid are the rails every claim in America still runs on. It is the foundation every later rule was built on.

And the fragmentation grew on it. A standard can only settle what the two parties don’t fight about. HIPAA could standardize the form of the claim, since the form was never the fight; it could not standardize the price, because the price is the contest. So it standardized the form of the claim but never the price inside it - and a shared form only let the fighting scale. There are, depending on how you count, somewhere between several hundred and a few thousand health insurers in this country — national carriers, state Blues, Medicaid plans, the administrators running self-funded employers. And each one published a companion guide: the local quirks layered on top of the standard, the extra fields, the house rules, the one form refracted into hundreds of slightly different ones. Vendors productized the exceptions; the clearinghouses built whole businesses on the gap between the format two payers were supposed to share and the ones they actually used. In finance a clearinghouse exists to make settlement certain, netting the trades and guaranteeing the money; healthcare borrowed the name for a business that clears nothing - it translates the dispute and passes it along, because there is nothing underneath to guarantee. But the cracks — the price, the terms, everything the two sides actually fight over — were never built into it, and the fragmentation grew up through them.

The mistake was the same one price transparency would repeat a quarter-century later: it assumed the two sides were fighting because they could not understand each other. Get everyone speaking one language, the thinking went, and the friction falls away. But they were never fighting over language - two parties fighting over money do not stop fighting when you hand them a shared form; they fight more efficiently. A signage standard tells two drivers how to read the same intersection - it does not decide which of them yields.

Call it what it is

Picking apart the side effects of healthcare policy is a trope at this point, and yet we never examine the defining feature of American healthcare. Every rule in this essay circled the same thing. ICD-10 standardized the language around it, price transparency published the rates beside it, prior authorization put a clock in front of it, the No Surprises Act built a courtroom to fight over it. Each pressed closer than the last, never onto it, and the consequences grew with the proximity — more codes, more filings, more machinery for the dispute. What they skirted was the contention at the bottom: what the care was worth, and so what is owed for it — the disagreement a capitalist market cannot seem to nail down.

And price is more than just a number - it’s a deal closed before the work begins, and when two parties cannot close one, the deal dies there and both walk away. Healthcare’s parties can do neither. The hospital needs the insurer’s members, the insurer needs the hospital’s beds, and the network terminations that make the local news are theatrics before the re-signing. So the contracts get signed and the rates get settled, and the deal still never closes - a rate prices the code, and every claim re-opens whether this care, this code, this coverage earned it. Thousands of these pairings across the country keep re-arguing it, a few hundred dollars at a time, with the question underneath: what was that care worth, and what is owed for it? The provider cannot say what an hour of its work is worth; the payer will only name what it is willing to pay; decades on, the cost of healthcare continues to grow.

The dependence and the resentment are the same bond. So they fight the way a married couple fights - in public, in front of the kids, the same grievance in new words every round - and the rules in this essay are marriage advice: one shared language, open books, a timer on the answers, even a courtroom for the worst of it. They take all of it and stay married.

Only agreement would end it, and agreement cannot be set from above. Fix the price (flat fee, value-based rate, whatever the decade calls it) and the argument just moves to volume. This essay has no clean answer either; offering one would just add a forecast to the pile. The cases point to something narrower and harder: every rule assumed the basic question was already answered - that what is owed had been settled, and the rule only had to organize around it. It never was. There is no settled answer underneath, only the argument, and it has swallowed every rule written to end it.

Strip the fight down and it is two sides trying to narrow what care is worth and what anyone will pay - a negotiation that never closes. Running it — the coders, the denial software, the arbitration firms, the consultants (I was one) — gets counted as the cost of American healthcare, though the work is arguing, not care. The arguing alone (the billing, the back-and-forth with the insurer) was last counted at $471 billion a year, about a sixth of what the country then spent; administration taken whole runs a quarter to a third, rising with every new rule, because each one hands the fight another surface to happen on. The industry files it under overhead, as if it were friction in a complicated machine; it is the running cost of that open negotiation - and the least we could do is stop sending in the next regulator with the next rule and call it what it is: a permanent quarrel we built our largest industry to run on.

Reconsider the claim: a chronicle and a contention. The chronicle needed nothing from us. The contention — the assertion that a sum is owed — is what the country has spent thirty years governing: codified, compelled, circumscribed, convened, counseled - everything but concluded.

I was a young consultant at Deloitte then, doing what was essentially customer success work, trying to upsell client health systems on a pending ICD-10 deadline. We had access to client data and tailored slide decks that would show each system the revenue it stood to lose from coding mishaps - real numbers, their numbers, arranged to alarm. The problem was that the deadline kept moving (go-live slipped two years all told), and you could watch the alarm depreciate in real time: the first delay bought us urgent meetings, the second bought polite ones, and by the end half the client health systems had stopped caring about the deadline at all. Then the cutover came and went, the catastrophe didn’t, and the lesson the industry took wasn’t we prepared well - it was they cried wolf. That, I’d learn, is the standard arc of a compliance deadline in healthcare: announced as an asteroid, postponed into a nuisance, survived as a shrug, and remembered as one more reason to ignore the next warning.↩︎

Years later I was on the other side of the table, on an M&A project at a regional Blues plan that suddenly had two top priorities for the year: land the acquisition, and comply with TiC. The plan had a real data department - engineers, data scientists, people hired to build things a member might actually notice - and the roadmap bent around the mandate anyway. Integration work slowed. New product work slowed. The better ideas waited in line behind a compliance artifact, and the team spent its year building machinery whose only purpose was to satisfy the rule. The files went out on time, which got counted as the win; the real cost never appeared on an invoice - it was the year of better work that didn’t happen.↩︎

Texas tried to widen the door with its HB 3459 “gold card” law, which lets a physician skip prior auth once she has built a track record of approvals - reward the doctors who reliably order the right care and stop making them ask permission. A sound idea, except that only 3% of Texas physicians ever qualified. The exemption sits out of reach because, for the payer, the chokepoint is the point - friction deters orders, and a scan never requested is a scan never paid for.↩︎

It was a treat to look up stats about financial infrastructure... a great contrast to healthcare finance, and the magnitudes stop fitting in your head almost immediately. Fedwire’s $1.15 Quadrillion came in 217 million transfers - a daily average around $4.6 trillion, which means the Fed’s wire system moves most of a full year of American healthcare every business day. The securities clearinghouses settled $3.79 quadrillion the year before (roughly 715 healthcares); the card networks ran some 166 billion swipes for $11.9 trillion, every one of them a price agreed at a terminal in under a second.

Sources: Fedwire annual statistics, DTCC 2024 clearing volumes, NACHA network statistics and unauthorized-return cap, and SIFMA’s T+1 after-action report.

This holds for the commercial market; the public programs set their own rates outright. Value-based wonks will also point to capitation—a flat sum per head that settles owed in advance—but the country ran that experiment at scale in 1990s managed care, and revolted at what a pre-settled answer did to care. It runs again today as Medicare Advantage, where the plan still fights the hospital claim by claim; the fixed sum only moves the fight to volume, how many patients and how many days.

I was a young consultant at Deloitte then, doing what was essentially customer success work, trying to upsell client health systems on a pending ICD-10 deadline. We had access to client data and tailored slide decks that would show each system the revenue it stood to lose from coding mishaps - real numbers, their numbers, arranged to alarm.

The problem was that the deadline kept moving (go-live slipped two years all told), and you could watch the alarm depreciate in real time: the first delay bought us urgent meetings, the second bought polite ones, and by the end half the client health systems had stopped caring about the deadline at all. Then the cutover came and went, the catastrophe didn’t, and the lesson the industry took wasn’t we prepared well - it was they cried wolf. That, I’d learn, is the standard arc of a compliance deadline in healthcare: announced as an asteroid, postponed into a nuisance, survived as a shrug, and remembered as one more reason to ignore the next warning.

Years later I was on the other side of the table, on an M&A project at a regional Blues plan that suddenly had two top priorities for the year: land the acquisition, and comply with TiC. The plan had a real data department—engineers, data scientists, people hired to build things a member might actually notice—and the roadmap bent around the mandate anyway. Integration work slowed. New product work slowed. The better ideas waited in line behind a compliance artifact, and the team spent its year building machinery whose only purpose was to satisfy the rule. The files went out on time, which got counted as the win; the real cost never appeared on an invoice - it was the year of better work that didn’t happen.

Texas tried to widen the door with its HB 3459 “gold card” law, which lets a physician skip prior auth once she has built a track record of approvals - reward the doctors who reliably order the right care and stop making them ask permission. A sound idea, except that only 3% of Texas physicians ever qualified. The exemption sits out of reach because, for the payer, the chokepoint is the point - friction deters orders, and a scan never requested is a scan never paid for.

The reporting on Dr. Norman Rowe is wild… supposedly his own website prices a breast reduction at $15,000 to $25,000 - and who has billed as much as $440,000 for a single one through arbitration. Per the Times’ reporting: five biggest awards worth $1.4 million among them, a sixtieth birthday with 50 Cent and a cake shaped like his vintage Porsche, and a second specialty trademarked under the names Dr. Penis and Doctor Penis. His lawyer’s explanation for the win rate is the most honest line in the affair - arbitrators get reverse sticker shock, because they pay their plumber more to fix a toilet than the insurer was offering for the surgery.

... and one of the things that got hijacked in HIPAA? The National PATIENT Identifier. Providers got one - and a patient identifier WAS baked into HIPAA - BUT - congress prevented funding it.

HIPAA, Hi-Tech, No-Surprises, Pricing Transparency, Break-up Big Medicine, etc - these are all Kabuki Theater - designed to give the appearance of reform but they always falls short of the intended goal because the medical industrial complex can't afford systemic reform - and they are well-funded and heavily fortified to protect the status quo.

So - we're left to rearrange the deck chairs with piecemeal legislation that captures both our attention and our imagination - like all theater does - but leaves us forever addicted to "the tranquilizing drug of gradualism."