Fighting in Public

Watching hospitals and insurance companies make up or break up

The city has drama everywhere. Terry, my girlfriend at the time (now wife), and I strolled through SoHo and saw a classy couple shouting at the top of their lungs. Suit and cocktail dress, dressed for a night at Carbone’s — not squared up about to throw down outside a bodega. Everyone around them pretended not to hear.

I caught fragments of the fight. She said something like “You do this EVERY. SINGLE. TIME.“

He threw his hands in the air. “Then maybe I should just fucking leave?!”

It’s rude of me to eavesdrop. Terry tugged at my arm — a signal to keep walking: mind your own business. But I can’t help it; I’m a busybody, and I’ve heard this fight before.

Whatever happened that evening was just the thing that broke the surface. The actual fight was older than that. I always wonder what happens behind the scenes. Anyone in a relationship knows how heavy baggage can be.

People love public fights. We’ll speculate on celebrity divorces, political palace intrigue, pro athletes beefing with their franchises. What could have led to this?

Hospitals and insurance companies fight in public too. Louder, honestly — and with a lot more at stake. But the general public doesn’t really care. Most people do what Terry did: keep walking, mind your own business. But I can’t help it - I wonder what led up to this point.

Rules of Engagement

I bet the couple on the sidewalk didn’t set out to fight in public. Something had been simmering, and that night it boiled over.

Healthcare fights work the same way. For decades, insurance contract negotiations happened behind closed doors, in the privacy of conference rooms. Hospitals and insurers would exchange spreadsheets to support their rates, eventually find a number, and renew the contract. Patients never really cared to know.

But healthcare costs have become untenable. And it gets to the point where conference calls can’t contain it. That pressure has to go somewhere — so it spills into public view. Both sides lob shots through local news. Letters go out to patients warning them their doctors might not be covered anymore. Crisis communication firms get hired. There’s an increasing trend of public contract disputes. The public theater is just part of the process now.

“We learned it’s important to make sure that you’re telling your story before the payer does,” one hospital CFO said.

Why go public? Because it’s leverage. Hospitals set up patient advocates to help members do “just cause transfers” — switching insurance carriers mid-year, outside of open enrollment — when their doctors are about to fall out-of-network. When employers start getting calls from angry employees, when membership numbers start dropping, the insurer’s negotiating position changes. “When the payer starts to see their actual membership numbers change,” one hospital executive explained, “they approach the negotiation differently.”

Breaking Up

Out-of-network is the healthcare contract equivalent of a break up. When a hospital threatens to go out-of-network with an insurance company, even uninterested bystanders hear it, whether they know it or not. OON means the hospital loses its insurance contract and guaranteed patient volume. The insurer loses members who want that hospital.

We call these “contract disputes”, but that undersells it. These are negotiations for who gets to stay in the bundle. Think of a health insurance network like Amazon Prime Video — hospitals, doctors, and labs bundled together and sold to employers. When a show like Friends falls out of the catalog, you can still watch it, but now you’re paying $4.99 per season instead of getting it with your subscription.

Except when Friends leaves Prime, you just go watch it on HBO Max. When your hospital leaves your network, you might be renting each visit to your oncologist at OON prices — or switching doctors mid-treatment.

Even if they come to an agreement, they drag their fights out in public. Below are a list of disputes across the country in the past few years post-COVID.

Every one of those disputes meant lawyers on retainer, consultants managing the fallout, and staff fielding calls from patients asking if they need to switch doctors. When you notify patients that they might lose their hospital, you’re not doing them a courtesy. You’re creating pressure.

He Said, She Said

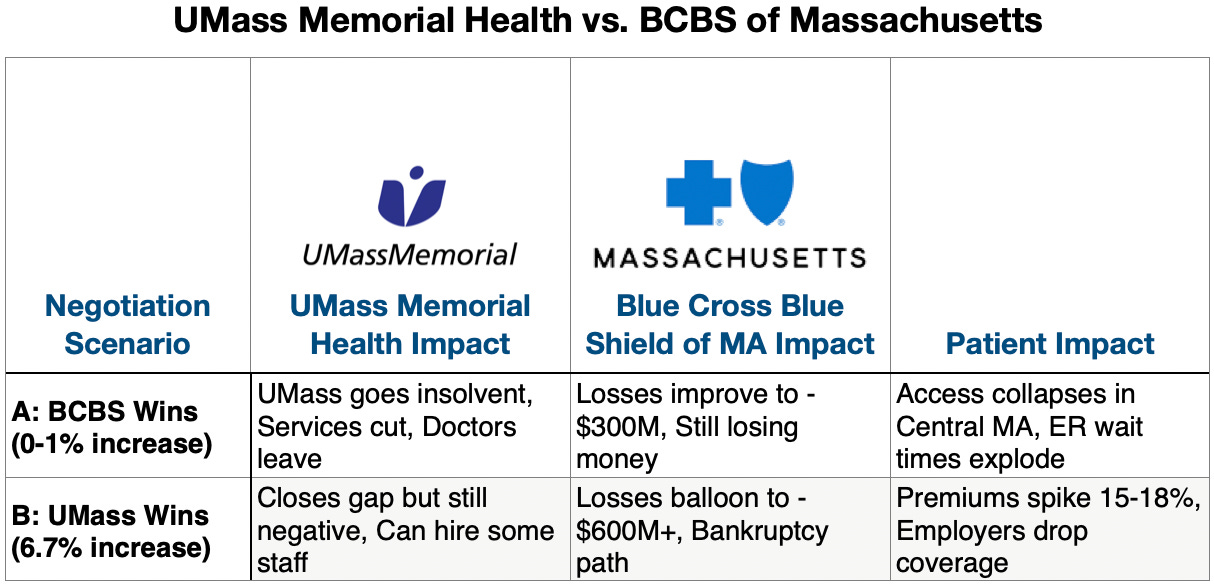

Last year, I watched one play out in my own backyard in Worcester, surprisingly the second-largest city in New England. The fight between Blue Cross of Massachusetts and UMass Memorial Health — the dominant insurer and the dominant health system in Central Mass — spent weeks playing out in public. Nearly 200,000 people waited to find out if they’d lose access to the biggest hospital in the region. A mother in Gardner got a letter reassigning her 16-year-old son to a clinician two hours away in Boston. “It’s just infuriating,” she told the Boston Globe. “I feel they are using us as pawns.”

UMass has the highest Blue Cross exposure of any hospital system in the state. Blue Cross sends 85% of its Worcester-area payments to UMass. Nearly 200,000 Blue Cross members — about one in five UMass patients — depend on this relationship working. This is a codependent relationship.

During the standoff, both sides did what they always do: lob shots through the press. Blue Cross said UMass charges too much and wanted a 6.7% increase. UMass countered that Blue Cross squeezes them on primary care rates. Each side accuses the other of being unreasonable.

There’s emotional baggage that causes people in relationships to act out. I like to think that no one sets out to be an asshole - there’s usually a reason why they act that way.

Blue Cross Blue Shield of Mass lost $400 million in 2024 — their worst year ever. They’ve since bought out 750 jobs, casualties of healthcare economics. UMass posted $86 million in operating losses in just the first half of fiscal 2025. And while it’s hard to conjure up sympathy for healthcare institutions, it has been an extremely unprofitable year for these two non-profit organizations.

But beneath the theater, both sides faced bleak futures.

If Blue Cross held the line at 0-1%, UMass faced insolvency. The hospital cuts services, doctors leave, and the only trauma center in Central Mass starts to collapse. If UMass got everything they asked for, Blue Cross’s spiral toward bankruptcy and premiums spike 15-18% — employers start dropping coverage entirely.

Spreadsheets don’t negotiate. People do — and these people had their backs against a wall.

This isn’t two organizations negotiating at arm’s length. It’s a marriage (technically a polygamous one, since both have dozens of other partners, but for the sake of this argument, they’re each other’s primary). A stressed one, where both partners are broke, neither can afford to leave, and the fight is about how to split bills they can’t pay.

The question with any stressed marriage: what’s keeping them together? And is it enough?

Every payer-provider dispute has a story like this underneath it. The headlines show the fight. But to understand why neither side could walk away, you have to understand how they got here — the choices that made sense at the time, the dependencies that built up slowly, the moment they realized they couldn’t leave even if they wanted to.

UMass Memorial: Absorbing Everything

UMass Memorial didn’t exist until 1998 - it’s younger than Google. Before the merger, Memorial Hospital and UMass Medical Center were crosstown rivals. They reluctantly merged out of fear of getting pulled into Boston’s gravitational pull.

“There’s nothing like the threat of a provider in Boston coming in to get two rivals to come together,” one executive said at the merger’s 20th anniversary.

That consolidation made sense: build scale before someone else builds it for you. But scale meant responsibility. UMass absorbed every struggling hospital within reach - HealthAlliance, Marlborough, Wing Hospital. Each one came with underfunded services, Medicaid-heavy patients, obligations the previous owners couldn’t afford. Revenue grew from $640 million to $4.1 billion, but so did the obligations.

UMass became the only major nonprofit left in Greater Worcester, the only Level 1 trauma center in Central Mass, the only academic medical center in the state outside Boston. UMass sees seventy percent Medicare and Medicaid patients - programs that pay below cost. The scale they built to compete became the cage they’re trapped in. That gap gets covered by commercial payers, and dependency on commercial payers to cover the gap means vulnerability. In Central Mass, that mostly means Blue Cross.

When Eric Dickson took over as CEO in 2013, UMass was near bond default. He’s an ER physician who still takes shifts, and he thinks like a trauma surgeon. His response to the 2013 crisis: 600 layoffs, sold off a hospital. “I’ve seen times with trauma patients where you have to take the leg to save the patient,” he said. “I felt that’s a little like what we did.”

Now the knife is out again. UMass lost $86 million in the first half of FY25. Dickson has closed clinics, shuttered a teen substance treatment center, ended behavioral health services. The trauma surgeon is still cutting because the patient is still bleeding.

“It’s going to get ugly the next three years,” he says. “I mean, I should have retired last year.”

UMass has its back against the wall - and they’re not the only ones. Hospital CEOs across the country are saying versions of the same thing. With increasing medical costs, Medicaid and Medicare getting slashed, and ACA subsidies getting cut, the outlook for hospital reimbursement looks grim.

Blue Cross Blue Shield of Massachusetts: Carrying Everyone

Blue Cross of Massachusetts ended up with a dominant, yet highly exposed position for the state. They have over 60% market share (!) in Mass, but have a member base designed to lose money. How could that be? A landmark 2006 paper titled “Roadmap to Coverage” helped make the case to cover uninsured populations. The paper was driven by Sarah Iselin, a policy wonk who worked with the authors to make the case that Blue Cross would help cover uninsured patients.

Massachusetts passed near-universal coverage in 2006 - the blueprint for Romneycare, which became Obamacare. Blue Cross had to absorb those newly covered patients, the ones with chronic conditions that other insurers avoided. They stayed nonprofit when other Blues went for-profit. Stayed local when others consolidated nationally. Those choices positioned them as the politically essential insurer — the one making coverage expansion work.

Sarah Iselin became Commissioner of the Division of Health Care Finance and Policy a year after the law passed - the regulator overseeing these negotiations.

Medicaid expansion states saw similar dynamics. Their Blues plans absorbed the populations no one else wanted. The insurers that stayed nonprofit, that stayed local, ended up with members who cost more to cover than they pay in premiums.

Blue Cross of Mass built a business model around populations designed to lose money, making themselves a politically valuable institution - even when the finances suffered.

The $400 million loss in 2024 was their worst year ever. GLP-1 drugs alone are projected to add $1 billion over five years. Post-COVID utilization never came back down. Hospital prices keep rising faster than premiums can follow.

Blue Cross can’t do what for-profit insurers do: exit unprofitable markets, narrow networks aggressively, design benefits to discourage sick enrollees. They’re stuck with the member base their market positioning created. Every new expensive drug hits them first. Every hospital that can’t survive without them becomes a hospital they can’t drop.

In 2023, Sarah Iselin became CEO of BCBS MA - the who pushed for coverage expansion, then regulated it as Commissioner, now runs the company that expansion depends on.

Healthcare has a tight loop. The people who build the systems end up inside them. Iselin helped create the model where Blue Cross absorbed expensive members in exchange for being politically essential. Now she’s negotiating from inside an insurer losing $400 million because that member base costs more than premiums cover. It’s not an easy position to argue from.

Let’s Stay Together

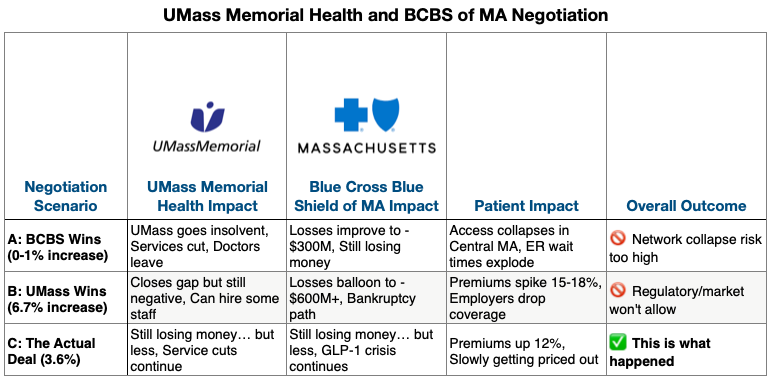

After months of public sparring, Blue Cross and UMass released a tepid announcement. They landed on a 3.6% rate agreement, which doesn’t make anyone really happy - but then again, a good compromise is when both sides are equally unhappy.

So why did they go through all that effort of airing it out in public? To understand why, let’s work backward again through the counterfactual scenarios.

Blue Cross could have held the line - offered 1% or nothing, forced UMass to take it or leave. But Massachusetts has some of the most aggressive network adequacy regulations in the country. An insurer that drops a region’s only trauma center doesn’t just face bad press - they face state regulators, employers asking why premiums pay for unusable coverage, and members leaving at the next open enrollment. It’s an existential threat for a plan that already lost $400 million.

If Blue Cross drops them, 200,000 members lose access to emergency care. Not “have to drive further” — lose access entirely. Patients caught in the middle of a fight they couldn’t control breathed a sigh of relief when the deal was announced, but months of uncertainty had already taken their toll.

UMass could have held out for 6.7%. But Blue Cross represents 35% of their revenue. For a system already $86 million in the red, walking away means bond default. Dickson already closed the clinics, ended behavioral health. The next round of cuts hits the trauma center itself.

So both sides were negotiating inside a very narrow band. Too low, and UMass collapses. Too high, and Blue Cross’s losses become unsurvivable. They found a number that kept them together... whether times are good or bad, if I’m happy or sad...

Every Couple Has Their Reasons

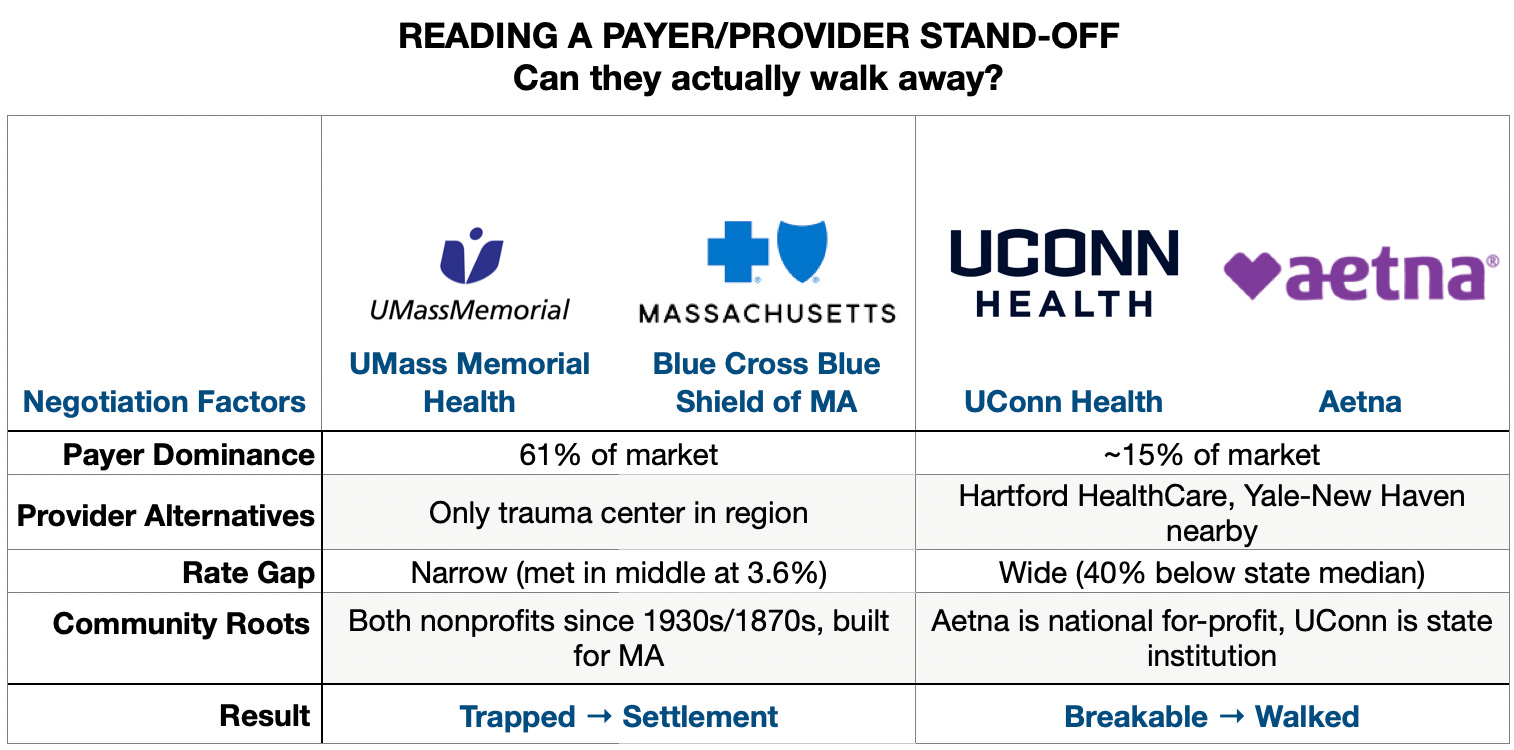

People in Massachusetts breathed a sigh of relief when UMMH and BCBS MA made up - but just an hour away across the state border, UConn Health and Aetna couldn’t close a gap.

Maybe it’s a morbid curiosity, but I spent a few months tracking these disputes. Every hospital juggles contracts with multiple insurers. Every insurer negotiates with every hospital in town. It’s hard to know the nuances of every market, but relationship patterns have two variables: can either side walk away, and how far apart are they.

When one side has alternatives, they use them.

The case for UConn and Aetna follows the typical “he said, she said”: UConn wanted higher rates, but Aetna said those rates would drive up costs for employers. Neither budged and the contract expired, leaving 15,000 patients out-of-network.What was the difference from UMass/BCBS? UConn Health is a single academic center in a state dominated by Hartford HealthCare and Yale New Haven. Aetna had alternatives — Hartford Hospital, Yale, a dozen community hospitals happy to take the volume. When an insurer has options, losing one hospital is manageable. UConn didn’t have enough leverage to make walking away hurt. So Aetna walked. First Connecticut insurer/hospital dispute to extend past deadline in recent memory.

When neither side can afford to walk away, even huge gaps close.

In my old stomping grounds in NYC, Memorial Sloan Kettering and UnitedHealthcare went into some brinksmanship right up until the deadline fighting over a 30% rate increase. MSK said United’s rates didn’t cover rising costs. United said 30% would add $400 million in costs by 2027. Neither side had a good exit. MSK is where you go for cancer in Manhattan. United couldn’t tell 19,000 cancer patients to find another oncologist.They settled just after midnight, hours after the contract expired. But when neither side can walk, someone blinks.

When there’s a power imbalance and the gap is too wide, someone gets hurt.

In Oregon, Salem Health demanded a 35% increase in 2025 plus another 15% in 2026. Regence offered 3.4%, citing Oregon’s healthcare cost growth target. Salem is the only hospital in town — which should mean leverage. But when you’re ten times apart, leverage doesn’t matter. It just feels like you’re asking too much.They broke up and 30,000 Regence members lost in-network access. After this acrimonious divorce, Salem started canceling patient appointments - the equivalent of taking our marital disputes on your kids. Oregon regulators stepped in to ensure continuity of care for 900 members mid-treatment, but mostly stayed on the sidelines. The state’s cost growth target gave Regence political cover to hold the line. Salem’s monopoly position wasn’t enough.

Divorce is contagious - and the trend is expected to grow. Everybody got along during COVID, but higher utilization and expiration of subsidies created an environment of contentiousness in a post-COVID world. That’s why you see increases since 2021. Most recently, a high profile case is how Johns Hopkins has been out-of-network with United since August. Duke is threatening to leave Aetna in North Carolina. Nearly one in twelve hospitals had a public dispute with an insurer between 2021 and 2025.

The Data Behind the Drama

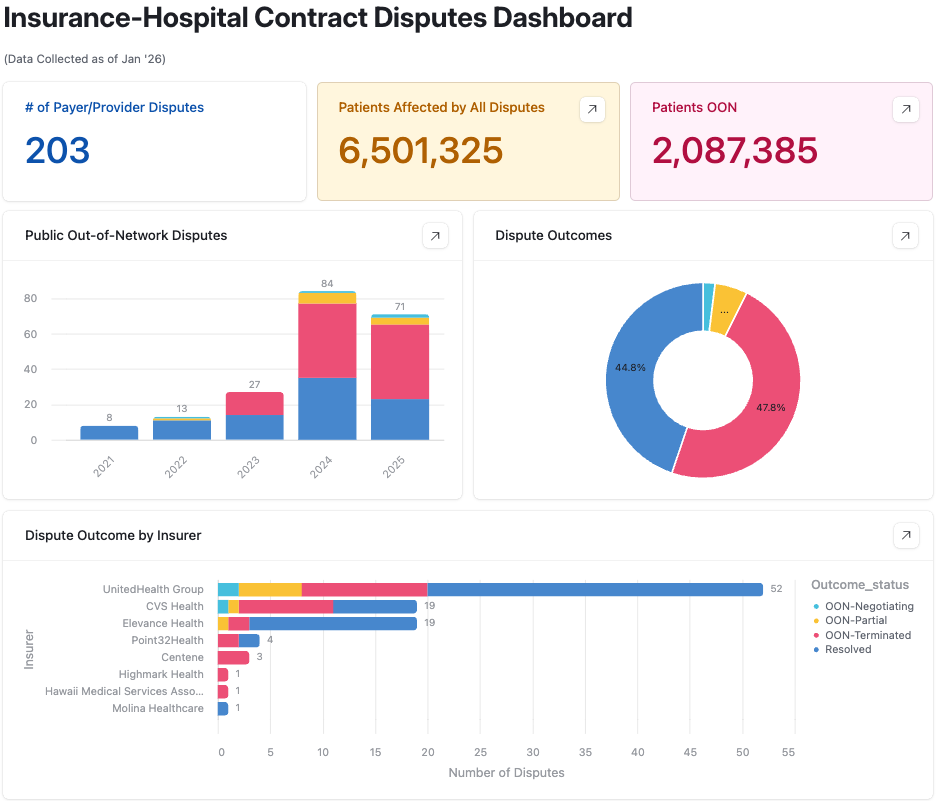

I’ve captured 200+ disputes so far, affecting over 6 million patients across 38 states. The data is messy — some disputes get national coverage; others I only find buried on page six of a regional business journal.

Here’s a link to the Airtable (I think I should start charging for this data)

It’s like watching a couple fight on the sidewalk. I can’t look away. I built some research agents to track the press releases, local news stories, state insurance filings - a record of the healthcare institutional drama leaving lives at stake. The hospital, the insurer, the stated gap, whether they settled or divorced, how long it took.

The map below shows where these fights are clustered. Texas. California. The Northeast corridor. Zoom in and you’ll see the names: Cedars-Sinai and Anthem. Ascension and United. Regional systems you’ve never heard of, fighting insurers you have.

The data might predict whether they stay or walk away, but human nature shows that the couples who can’t leave find a way, the ones who can walk often do, and the gap determines how bloody it gets. The stories underneath are still being written — and I’m still adding to the database (feel free to check it out and let me know what’s missing/inaccurate). Hover over the circles to get more info of each dispute.

More Fights Coming

Financial stress is the number one predictor of divorce in real marriages. Hospitals and insurers across the country are telling the same story: it’s their fault, something has to give.

We’ve seen this before. The last wave hit around 2000, when hospitals first consolidated enough to say no. In 1996, zero major contract disputes — hospitals took whatever terms insurers offered. By 2000, contentious disputes had erupted in 7 of 12 markets studied. That backlash faded. Now the pressures are different — Medicare Advantage, GLP-1 drugs, post-COVID labor costs — but the dynamic is the same: pressure builds, leverage shifts, negotiations go public.

Not every couple will make it. Sarah Iselin’s prediction: “I don’t think every hospital that’s open right now will be open in five years.” The patients who depend on those hospitals won’t get to choose which ones.

Staying Together

Breaking up is hard - staying together can be just as hard. UMass and Blue Cross stuck it out, but both sides are still losing money. And who bears the brunt? The 200,000 members who need that trauma center, but will see their premiums get taken out of their paychecks. When married couples fight, the kids are the ones who get hurt.

I grew up watching my own parents fight. I learned early that sometimes couples stay together not because they’ve resolved anything, but because leaving would hurt the kids more than staying.

In the end, I think that these conflicts aren’t going to be going away. It’ll probably get worse based on what we see in the trends. But I just hope to understand them a little better, to get a better sense of empathy for all of those involved in the drama.

Great coverage - which I also stabbed at back in 2012 for Forbes:

https://www.forbes.com/sites/danmunro/2012/03/30/when-healthcare-titans-compete-patients-lose/

Back then it was UPMC and Highmark playing out their decades old battle. Sadly - not much has changed - nor is it likely too - except that it's becoming even more prevalent.

Sadder still is how much of the patient view is lost in these battles for revenue. Public rates are too low - so the commercial side has to carry *everyone* to profitability - and who funds that? Employer Sponsored Insurance - which covers about 160M Americans - and commercial rates are just INSANE. The average cost of ESI coverage for a Family of 4 (PPO coverage) is over $30,000 - per year. That's average.

We keep saying all this is unsustainable - but that's a lie too because nothing will change unless/until we end ESI (and cap commercial rates). We could do that. We should do that - but the change has less to do with healthcare and more to do with tax reform and *that's* not likely anytime soon.

http://hc4.us/esi20

Well done as always. Have you found the Healthcare uncovered substack /crew yet?