The Office Birthday Cake

Who decides why employer-sponsored health insurance is so expensive, explained with cake

3.3k words, 13 min read

The office birthday cake is a relic of the before-times, when we all used to work in the same building. Deb from accounting’s birthday is coming up, so somebody sets up a Venmo, everyone chips in five bucks, someone picks up a sheet cake, you sing in the break room, and Deb gets her moment. And unless you work at Dunder Mifflin, it’s a low-stakes process that costs forty dollars of sugary frosting.

For years I was happy to chip in a few bucks whenever someone’s name came up on the calendar, vaguely pleased when it was my turn and someone brought something with whipped topping. The ratio of people-to-cake was more than enough for me.

But now scale that up. Instead of Deb’s birthday, the office chips in when someone’s baby arrives three months early, and the NICU bill hits $2M. Or when someone’s spouse gets a cancer diagnosis that requires a drug costing $15,000 a month. Or a new hire at the office — you’ve said hi passing her in the hallway (but don’t remember her name) — starts a Wegovy prescription at $1,000 a month because her doctor said her BMI qualifies. You’re no longer splitting a sheet cake, but you’re paying for it.

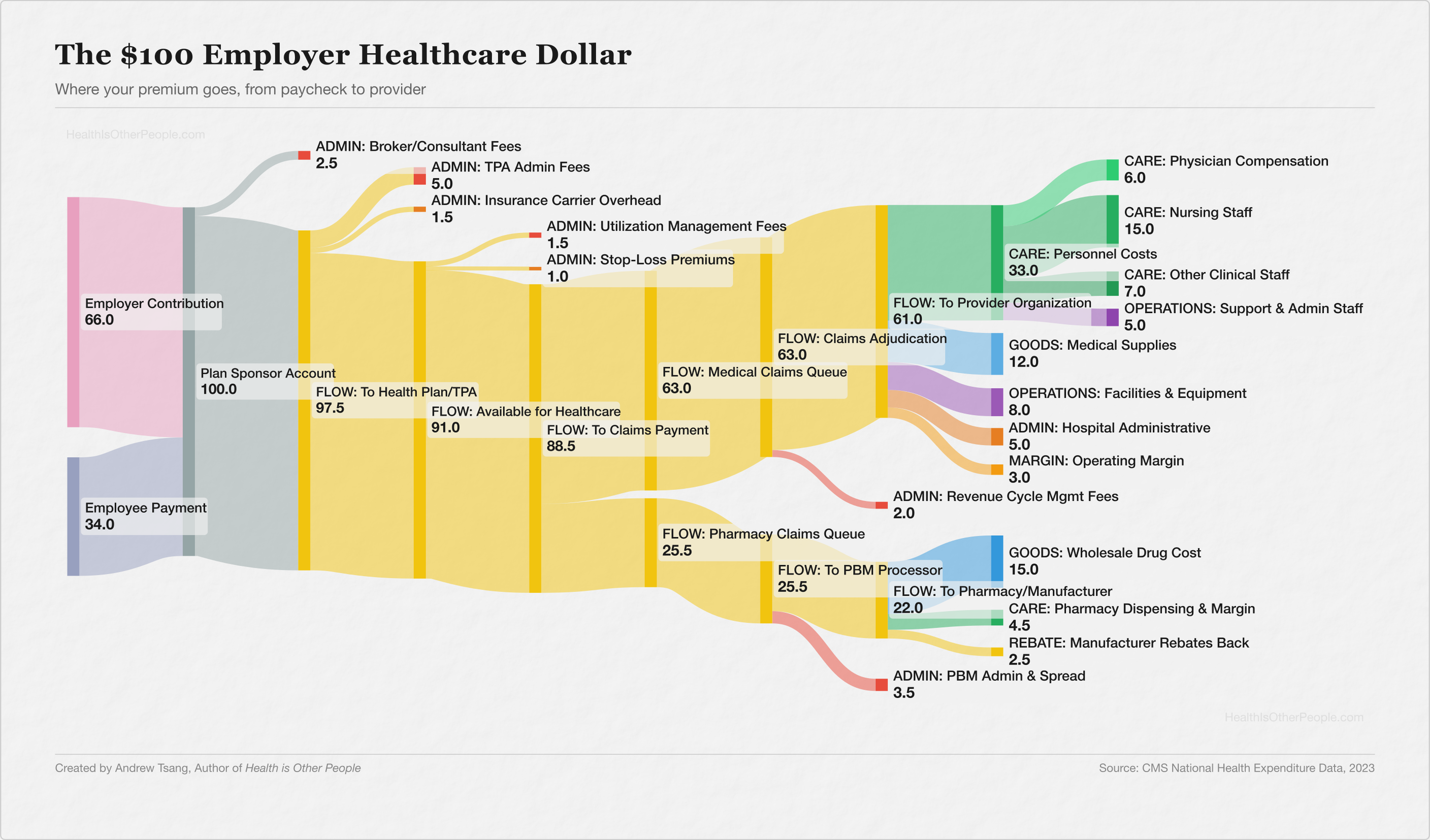

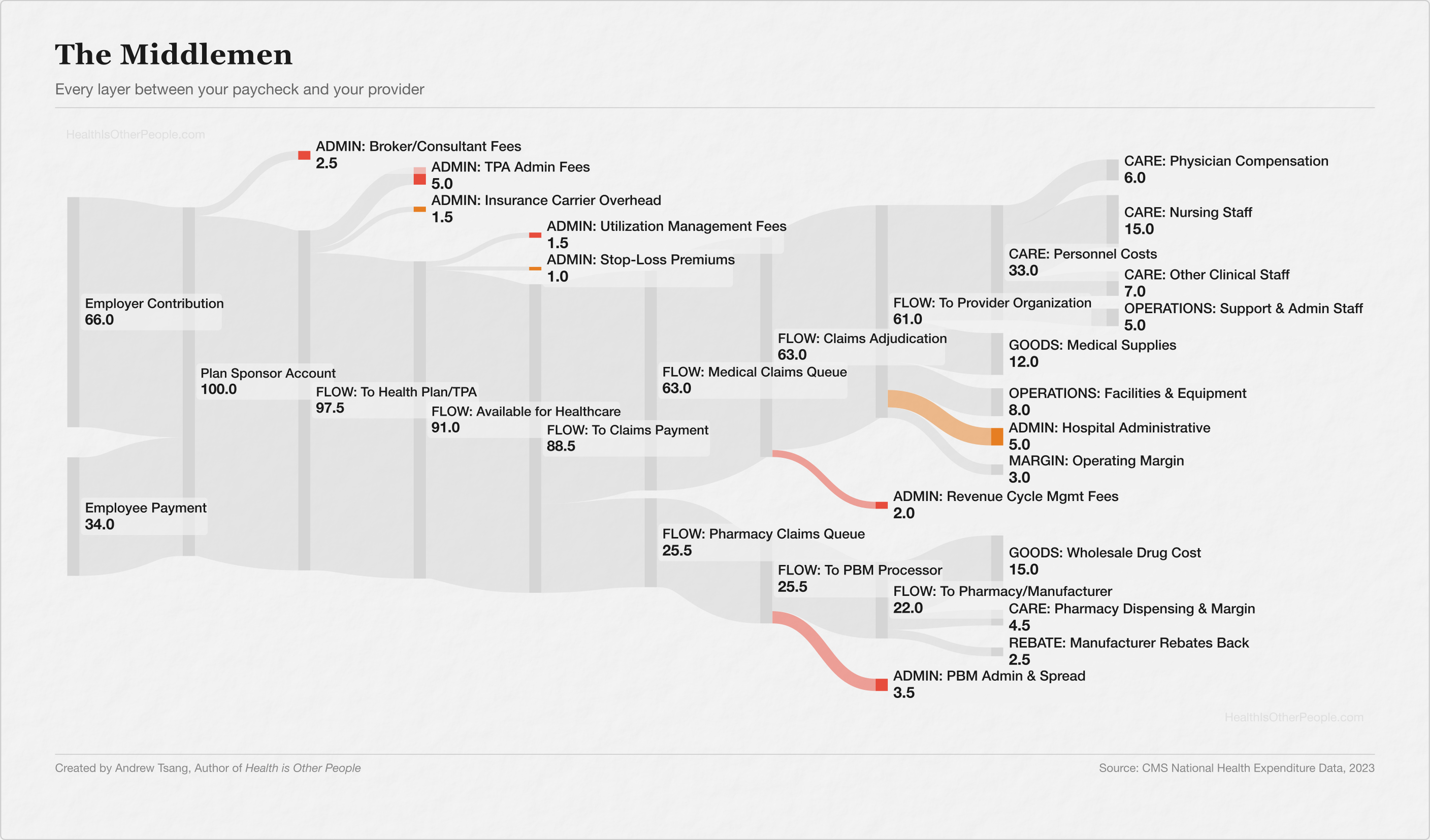

If you've had a job (and I presume you do, to read this on the Internet), at some point you got a 1095-C in the mail, had some money taken from your paycheck, and never thought much about what connected those two facts. As a once-young and still-healthy man, I hardly used my benefits. I was simply happy enough to have a salary and a card in case something bad happens, and never thought about where the money went. But then I became the head of a family and saw my precious premiums proliferating. In 1999, the average family premium was $5,791, which was roughly the cost of a used car. In 2024, it was $25,572 — roughly a new car. Premiums have outpaced wages 3-to-1 over that period. And most of the money disappears into a loop between your paycheck and your doctor that's surprisingly hard to trace. I wanted to know what I was paying for. So I traced it using my patented Tsang-key diagrams :

Between your deduction and your employer’s contribution — which, for most companies, runs 2x to 3x what comes out of your check — I counted eight to ten separate companies handling that money before it reaches your doctor, depending on where you draw the lines.

For every $100 your employer spends on your healthcare, roughly $16.50 goes to administrative processing before a dollar reaches anything clinical1 — the brokers, claims administrators, carriers, utilization managers, pharmacy benefit managers, and revenue cycle firms that sit between your premium and your doctor. Those fees look small on their own — a broker takes 2.5%, the claims administrator takes 5%, the carrier skims 1.5% — but they stack, and each one operates independently, its own approval process, its own software, its own timeline. Six steps between “your doctor says you need this” and “you get it.”

The biggest slice, $39, goes to the people who deliver care — but most of that isn’t your physician. It’s nurses, technicians, therapists, the intake coordinator who checks you in, the clinical workforce that keeps a hospital running twelve hours after the doctor goes home. Another $27 goes to drugs and supplies, $14 to facilities and equipment, and the hospital keeps about $3 in margin.

Healthcare is a funny industry — with payers, providers, and pharma believing they’re the good guys getting squeezed by everyone else. After mapping this, I get why: the incentives point in different directions at every layer. I went in expecting to find a villain, one layer extracting more than its share. Instead, I found a chain of answers to the same question: “Who decides what the money is for?“

The principle hasn’t changed since the first office collection — everyone chips in so the money’s there when something goes wrong. Who should pay when someone gets catastrophically sick? Since 1943, the American answer has been: your employer. Not the government, not the individual, not the community — your employer, because during the war, the government froze wages, companies offered health benefits instead, the IRS decided not to tax them, Congress made it permanent, and a wartime workaround became the single largest tax expenditure in the federal budget — $300B a year in foregone revenue. Employer-sponsored insurance covers more Americans than any other source — 160 million people, more than Medicare and Medicaid combined.2

And because those health dollars are tax-free — for both employer and employee — every dollar routed through the plan buys more than a dollar of wages. Congress tried to cap it once (the Cadillac tax), but it was delayed four times and repealed in 2019 before it ever took effect. The system doesn’t just spread the cost — it rewards spending more, routing more compensation through the cake instead of the paycheck.

Buying the Cake

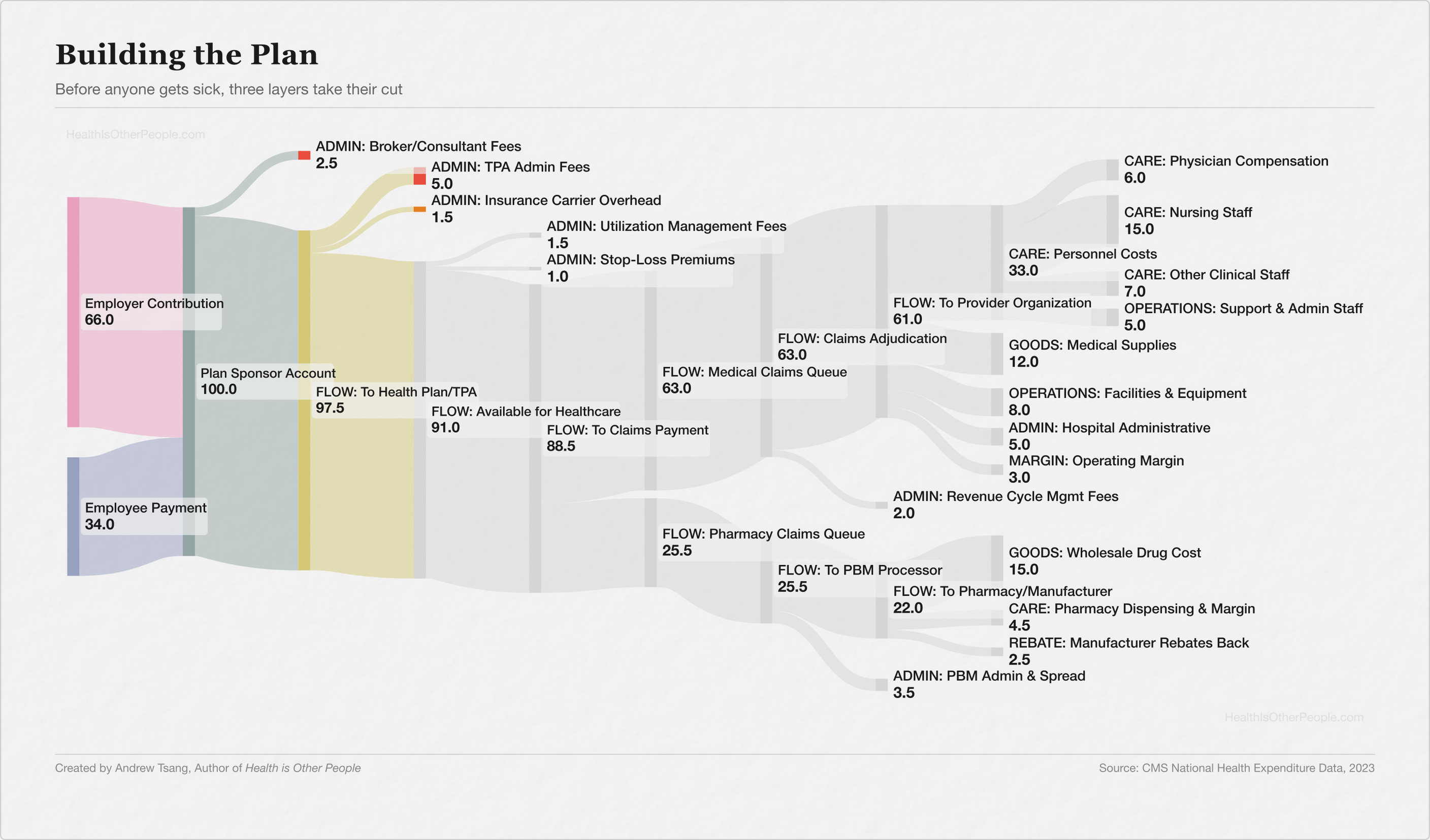

So the pool exists, and someone has to manage it. Most large employers self-fund — keep the premiums, pay claims out of operating funds, and hire a third-party administrator (TPA) to handle the paperwork: processing claims, building the provider network, mailing the cards, answering the phone when you call the number on the back. The TPA runs the plan day-to-day for about 5% of premium, instead of the 15-20% a fully insured carrier keeps. Two-thirds of American workers with employer coverage are in self-funded plans. But self-funding means your company’s HR department is now, functionally, running an insurance company — and most HR departments didn’t sign up for that, which is how you end up hiring the next layer.

The biggest brokers — Marsh McLennan, Aon, Gallagher — are publicly traded companies running the shopping layer for thousands of employers, handling the RFP process, presenting carrier options, benchmarking costs, and managing compliance. A mid-size company might pay its broker $50,000 a year in commissions. A large employer group can generate up to $150,000 in additional carrier bonuses on top of that — bonuses that, until 2021, the employer never saw. When one person’s recommendation steers millions in premium revenue, the carriers have every reason to make that person’s life pleasant.

ProPublica documented an arrangement in 2019: carriers using cash bonuses, Super Bowl tickets, and Bermuda resort trips to steer broker recommendations. When they asked the ten largest brokerage firms whether they accepted these bonuses, four declined to answer. Six never responded.

When I was researching this, my first thought was that I’d picked the wrong career. I’ve spent years working in hospitals and insurance — no one ever sent me to the Super Bowl. But it’s not uncommon: I worked on integrating a dental insurance product into a new sales process, and the brokers who sold the most got a free week-long trip to Ireland. Every VP on the call had a jealous little chuckle that they weren’t getting comped a free trip to Europe. The perks suggested a margin that the rest of healthcare hadn’t figured out how to capture.

A broker’s commission is a percentage of premium — when premiums rise, the broker makes more, with no built-in incentive to bring costs down. But without a broker, most employers are negotiating blind in a market designed to be opaque.

Each layer of the cake — the broker navigating the market, the administrator running claims, the carrier managing the network — took on a question the pool couldn’t answer on its own. Each answer costs a fee. But the plan is built now, the managers are hired, and those fees only matter when someone actually uses the pool — when the money has to move.

The Last Slice

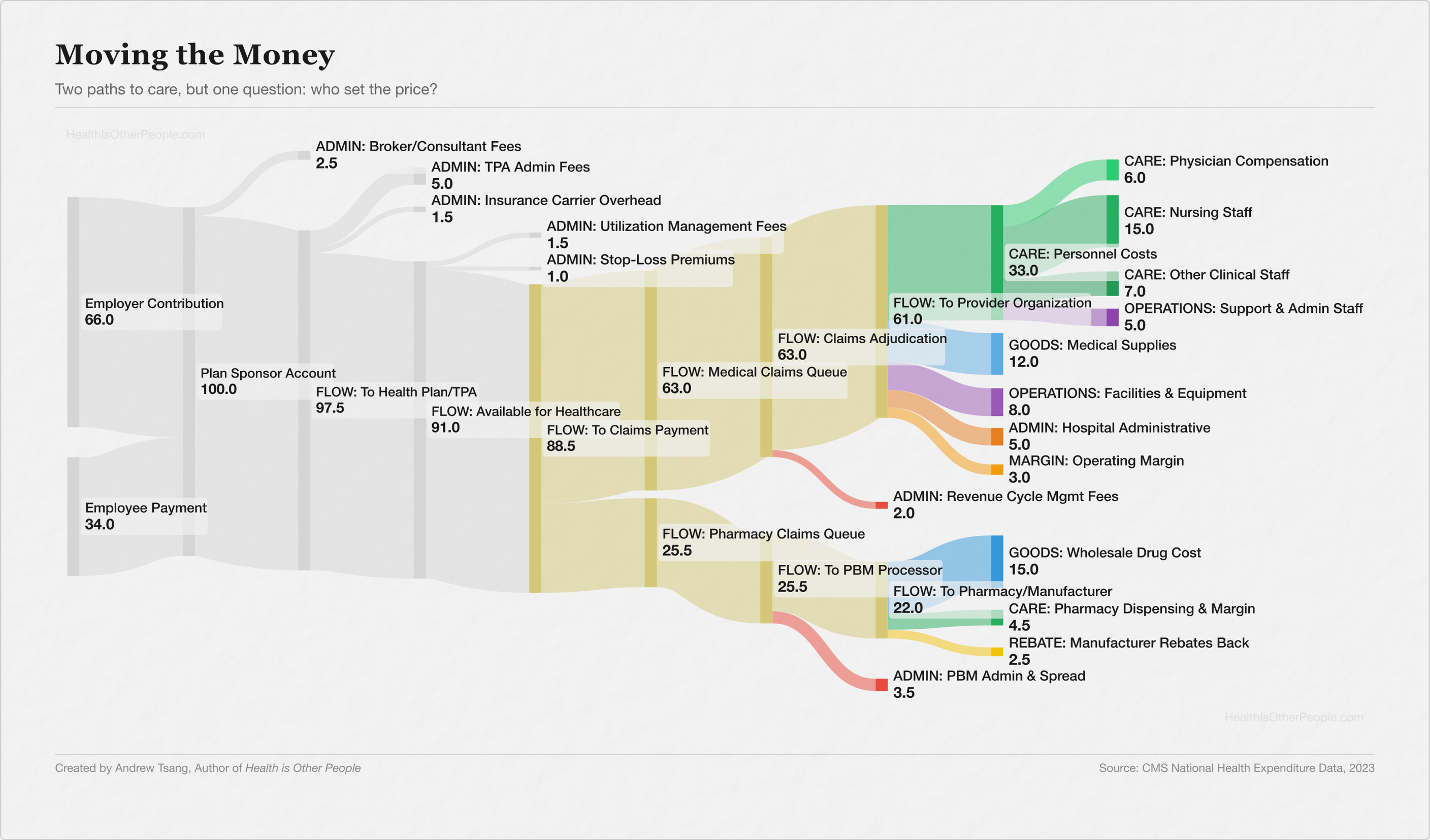

Every claim starts with the same thing: a doctor orders something, and a patient should get it. Between those two points, someone turns the order into a billing code, formats it to a specification, routes it to the right payer... and waits. Thousands of payers, each with its own formatting requirements, its own submission portals, its own adjudication rules, and a layer of clearinghouses translating between them — the rails of the system, running on a standardization problem that was supposed to be solved decades ago.

Getting paid is its own industry. Revenue cycle management — submitting claims, posting payments, fighting denials — is a $61B market, projected to hit $100B by 2030. U.S. hospitals spend 25% of their total budgets on administration — $667 per person in America — compared to 12% in Canada, where there’s one payer and one set of rules. The bakery is spending a quarter of its budget figuring out which office sent the five bucks.

Then there’s the drugs.

PBMs — pharmacy benefit managers — started as claims processors. You handed a card to a pharmacist, the pharmacist submitted the claim, the plan paid the bill. A transaction layer, no different from a credit card company skimming a processing fee.

Today, three companies — Express Scripts (Cigna), CVS Caremark (CVS Health/Aetna), and OptumRx (UnitedHealth Group) — control roughly 80% of the pharmacy benefit market, covering 270 million lives and managing $600B in annual drug spending, each vertically integrated with its parent insurer. The same parent company that insures you manages your drug benefits and fills your prescriptions through its own mail-order and specialty pharmacies. One entity decides what’s covered, negotiates the price, and captures the margin at the pharmacy counter — choosing the bakery, setting the recipe, and pocketing the difference between what the cake costs and what you’re told it costs.

The FTC spent years investigating and found $7.3B in profit from specialty generic markups alone, $1.4B in spread pricing — charging the plan one price, reimbursing the pharmacy less, pocketing the difference — and a rebate structure where higher list prices meant more money flowing through the PBM. The opacity is the business model.

In September 2024, the FTC sued all three for inflating insulin prices through exactly this mechanism.

But every wealthy country has drug intermediaries — Japan has more individual payers than the United States and a fraction of the overhead, because Japan set the prices.

Every pool in the United States negotiates separately — with every hospital, every manufacturer, every pharmacy chain. No standard rate for an MRI, a hip replacement, a vial of insulin. The same procedure, performed in the same city, billed at wildly different prices. It depends on which pool your employer built and which network your carrier negotiated.

Why didn’t we just set the prices?

Moving the money costs money, more every year, and most of it happens where you can’t see it. Does every dollar leaving the pot actually need to leave — and who gets to decide?

Who Ordered This?

Every October it’s the same ritual: open enrollment, premiums up again, the plan costs more, the deductible creeps higher, and at some point you stop shrugging and start wondering who’s reaching into the pot.

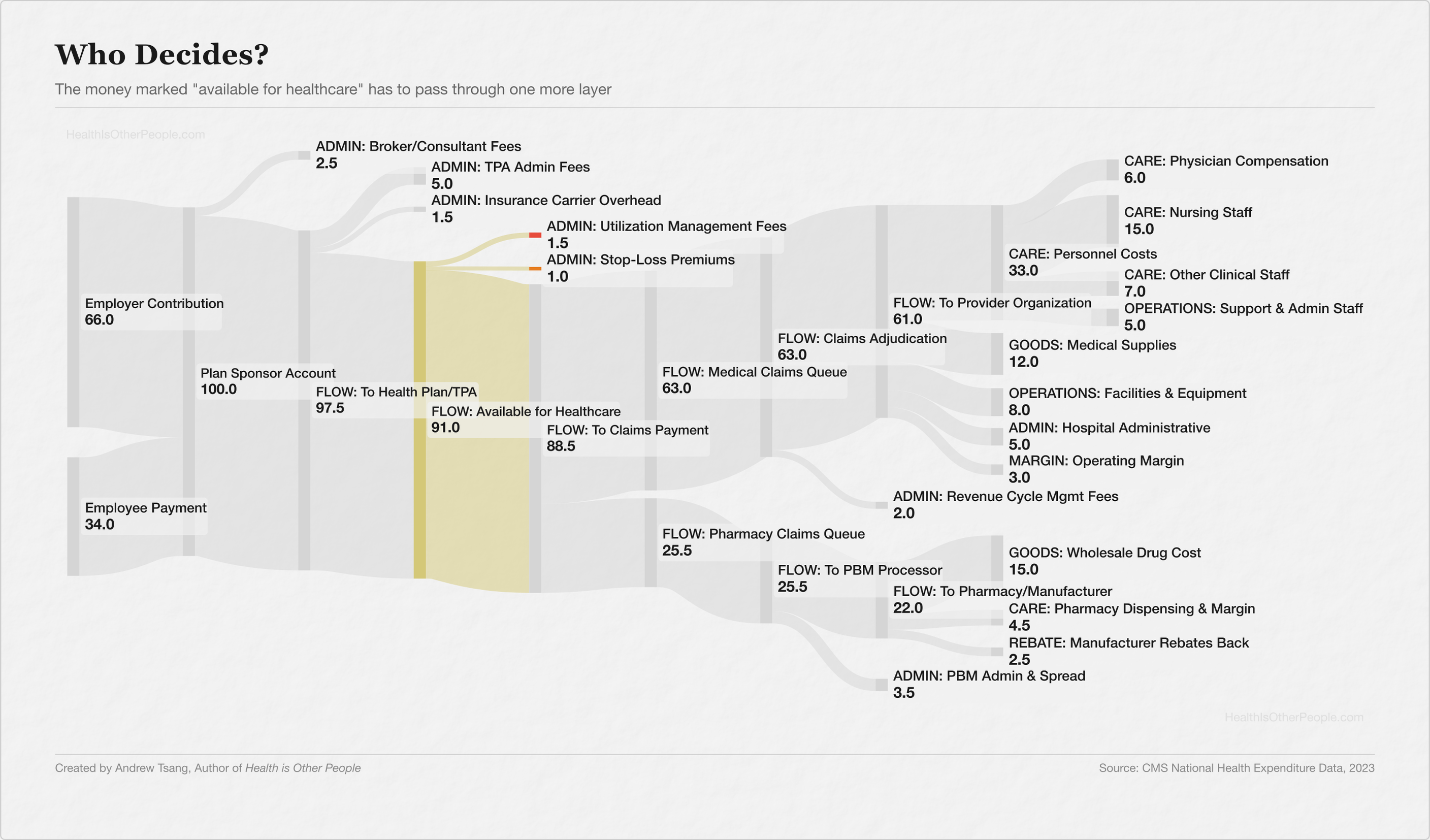

Prior authorization — getting permission — is a straightforward way to gate the money draining the pool. For decades, doctors would do more, bill more, then earn more. But with prior auth, before a doctor orders an expensive test, a surgery, a specialty drug, someone reviews the request against clinical criteria and decides whether the pool should pay. A checkpoint between the physician’s judgment and the pool’s wallet.

And it makes sense, in the same way the birthday cake made sense — if the pot is collective, everyone’s money, then somebody has to be the steward, somebody has to check the receipt before the bakery charges you for three cakes when you ordered one. Roughly a quarter of U.S. healthcare spending is wasteful — duplicative, low-value, or clinically unsupported. If prior authorization catches even a fraction of that, it’s doing its job.

Except.

Your carrier subcontracts the approval decisions to utilization management companies — firms your employer has probably never heard of, operating on platforms your employer has probably never seen, deciding case by case whether the pool pays for your MRI, your specialist referral, your kid’s therapy. Your employer built the plan, the carrier promised to manage it, and someone three contracts removed says yes or no. The total annual cost of running this approval layer — across all payers — is $35B.

I was on a Teams call at an insurance plan, helping write eligibility criteria for an advanced therapy, and all I could think about were the hours I’d spent on the provider side proving patients met criteria just like these.

The gatekeeping function makes sense — a quarter of U.S. healthcare spending is genuinely wasteful, and doctors will tell you privately that defensive medicine drives a significant volume of unnecessary orders. But 88% of physicians say that prior authorization increases overall healthcare resource utilization, through delays that escalate conditions and workarounds that route patients to more expensive settings. The honest answer from the research is that it’s unclear whether the checkpoint saves more than it costs, and no one has stopped doing it long enough to find out.

And stopping would mean someone at your company — an HR director, a benefits committee, a colleague you eat lunch with — has to look at a claim and say no themselves.

But when the gatekeeper says yes — when the claim goes through, the surgery is approved, the drug is covered — and the bill is $4M, somebody has to absorb the hit. There are 38 FDA-approved gene therapies, up to $4.25M per treatment, with over 2,000 in the pipeline. One diagnosis can drain the pool.3

Everyone’s Cake

You get your 1095-C, you start paying for health insurance. Down the hall, a hundred other people check the same box — the guy by the window with four kids who may need braces, the woman who just came back from medical leave for a private reason, the new hire no one’s met yet. All of you, paying into the same pot. So when something goes catastrophically wrong for one of you, the money’s there.

That’s all insurance ever was — everyone chips in for the cake.

But your pot doesn’t stay in your office. Your employer’s pool — your premiums, your coworkers’ premiums — merges with thousands of other employers’ pools inside the same carrier’s book. UnitedHealthcare covers 50 million people. You’re in a pot with auto workers in Michigan and hotel staff in Phoenix, people you’ve never met — your money paying their claims, their money paying yours. And at the hospital, the pools dissolve completely — there’s no UnitedHealthcare wing and no Aetna wing, just beds and doctors and everyone converging in the same building.

With catastrophic claims, we pool risk again with other employers’ catastrophic risk, and a reinsurer bundles it again into global capital markets, so a gene therapy claim in Ohio ends up as a line item on a balance sheet in Munich.

And then there’s the biggest pot of all, the one that doesn’t even look like insurance — $300B a year in foregone tax revenue. The employer health coverage exclusion basically means every taxpayer in America subsidizing the system whether they’re in it or not. The pot was never your office, and the tax code has been telling your employer to make it bigger every year.

The Receipt

We blame the middlemen — the PBMs, the utilization managers, the brokers collecting Super Bowl tickets — for making the system expensive (and they do). But they’re expensive because we hired them, and the tax code rewards every dollar we route through them.

We built every layer between our paychecks and our doctors because we couldn’t look at each other and decide what the money’s for — the broker so we don’t have to shop, the carrier so we don’t hold the risk, the UM company so no one has to say “no” to a coworker’s face. The 16.5 cents of frosting on every dollar is what it costs us to not decide — enough layers that when something goes wrong, the denied treatment, the surprise bill, the delay that costs someone their life, every entity can point somewhere else.

It’s meant to be morally provocative: a $4M gene therapy for a colleague’s child — should the pool pay for that? A $1,000-a-month Wegovy prescription for a coworker you barely know — should it pay for that? An 82-year-old employee who wants the freedom to choose her own hospital, even if the out-of-network option costs the pool twice as much — should it? These aren’t questions with clean answers, and I think the tension is that we don’t like that we’ve deferred the answers to someone else rather than confronting it ourselves.

Just Desserts

I’ll be honest, all this stuff is hard to confront — it’s so convoluted, and now there’s this huge moral entanglement on top of it, that the decisions we make about each other’s coverage actually matter for the people we work with, and it’s bizarre to me that we don’t really talk about it. But one organization did it.

I caught a wonderful podcast episode of Trade-offs, which showed a company running into the problem of making decisions on health benefits. It’s a bold, and empathetic, way to think about the morality and feasibility of managing employee benefits.

They gave employees 70 poker chips representing the health budget and said: the full plan costs 92 chips, you can’t have everything, decide together. Not by vote — by consensus. Every person in the room had to agree, which meant every person in the room had to listen.

They read scenario cards — the cancer treatment, the weight-loss drug, the fertility coverage — and talked through what the shared money should cover, out loud, with the people whose money it was. They declined Wegovy. They approved infertility treatment. A younger employee changed her vote after hearing an 82-year-old colleague explain why hospital choice mattered to her. The empathy wasn’t just a moving patient story — it came from sitting in a room with the person whose coverage you’re deciding.

One group voluntarily chose to reduce their own salaries to buy more coverage once they understood the constraints. 85% liked the outcome. The NPC published a case study, Health Affairs covered it, and the conclusion was what you’d expect if you’d been paying attention: when people sit in a room and make these decisions together, they accept the limits as fair, because they made them, looking at each other.

When I traced my $100 of premiums, and I wanted to know where the money went. I learned it went to everyone — to the coworker whose kid needed the NICU, to the colleague on Wegovy, to the retiree who wants her hospital — and the 16.5 cents of frosting went to making sure I never had to sit in a room and face any of them while it happened.

Health is Other People is (obviously) an allusion to Jean-Paul Sartre, and he called this mauvaise foi — or bad faith — pretending you don’t have a choice when you do. The original sin of America’s employer-sponsored insurance is that we assumed there was no way out. It’ll stay this way until we sit down and ask, “what do you want it to cover?”

Anyway, open enrollment is in October. You’ll get the email, you’ll compare two plans you don’t understand, you’ll pick the one that costs slightly less, and somewhere between your paycheck and your doctor, ten companies will collect their slice. The cake, at least, is tax-free.

The $16.50 Methodology: This figure aggregates published cost estimates for each intermediary layer in the employer premium dollar: broker commissions (~2.5% of premium, per KFF and industry disclosure data under the Consolidated Appropriations Act), TPA/ASO administration fees (~5%, per Georgetown CHIR and industry fee benchmarks), carrier ASO fees (~1.5%, per Health Affairs, median $190-$225/enrollee/year), stop-loss premiums (~1.5%, per IFEBP at high attachment points typical of large employers), utilization management (~1.5%, derived from the $35 billion in total PA administrative costs apportioned to employer-sponsored coverage), PBM administration and spread (~3.5%, derived from FTC findings on markups and spread pricing relative to employer drug spend), and revenue cycle management (~2%, derived from market sizing relative to total employer health expenditure per CMS). Each component reflects a range; the aggregate is an estimate, not a published figure. The Tsang-key diagram above visualizes the full flow.

The MLR Paradox: The ACA tried to cap carrier overhead at 15-20% of premiums — the Medical Loss Ratio rule. Spend at least 85 cents of every premium dollar on medical claims, or rebate/pay back the difference. But the MLR is a percentage, not a dollar cap. When medical costs rise 20%, premiums follow, and the carrier’s 15% grows in absolute dollars without lifting a finger. Research from the American Economic Association found that carriers affected by the rule actually increased claims costs by 7-11%, achieving the ratio by letting costs rise rather than cutting overhead. After the vertical integration wave — CVS acquiring Aetna for $69B, Cigna acquiring Express Scripts for $67B, UnitedHealth building Optum into a $250B behemoth — most large carriers now own their own PBMs, provider groups, and specialty pharmacies. Payments to those subsidiaries count as “medical spending” under MLR. The money leaves the carrier’s insurance arm and lands in the carrier’s pharmacy arm. Technically compliant. The money stays in the family.

Stop-Loss — Insurance for Your Insurance: A self-insured employer paying claims out of operating funds has no ceiling on exposure. So you buy insurance for your insurance. Stop-loss sets a ceiling — if any single employee’s claims cross a threshold, say $500,000, the stop-loss carrier picks up everything above it. The stop-loss market doubled from $12B to $24B in five years, projected to hit $113.5B by 2034. “$3M claims are the new $1M” is something actuaries are saying without irony. But the stop-loss carrier isn’t blind — if your plan has an employee with a known expensive condition, the carrier can “laser” that person, setting a higher threshold or excluding them from the policy altogether. The employer still covers that employee’s claims out of operating funds, dollar for dollar, with no ceiling. Stop-loss protects the risk pool from the unknown catastrophe — the diagnosis no one saw coming. The known expensive patient is not a risk from the carrier’s perspective, but rather a certainty.

I at once completely agree with the core point and am picturing doing 12 Angry Men with 50+ colleagues every time we hire someone

Hey — I came across your writing and really liked how you think.

I’m exploring something similar from a different angle — writing about human behavior through a system design lens (like debugging internal patterns).

Just started publishing on Substack. If you ever get a moment to read, I’d genuinely value your perspective.

Also happy to support your work — feels like there’s an interesting overlap here.