The Gravity of Boston’s Healthcare

Or my alternate title “On the Red Line: Healthcare to a T”

I've always known Boston for its universities and championship-winning teams - not in that order. It's silly because I grew up in Massachusetts, and I've taken Boston's healthcare dominance for granted. It's arguably the best city for healthcare - yet a perfect illustration of the flaws in healthcare market dynamics.

Through my healthcare career, I marvel at Boston's world-class hospitals, cutting-edge biotech, advanced medical education, and abundant health research funding. Its excellence creates a gravitational field pulling in everything healthcare-related.

You can see the wealth of health by walking through the brick-clad buildings of the Longwood Medical Area neighborhood - home to world-renowned institutions like Boston Children’s, Brigham and Women’s, Dana-Farber, Beth Israel Deaconess, and Harvard Medical School - and see more medical firepower packed into a few blocks than many entire states.

Healthcare entities in a few blocks. Net revenue estimations.

This creates a self-reinforcing cycle. More med students mean more research, leading to more breakthroughs, attracting patients who believe Harvard-affiliated care is better. That patient volume lets academic centers charge higher rates and offer salary bumps to recruit top talent. Better talent attracts more NIH grants, funding more research. Clinicians, researchers, patients… all making rational choices that fuel this concentration of healthcare.

No doubt about it: this business of healing is great for medical innovation. These institutions create treatments and technologies that benefit people worldwide. Boston's medical ecosystem drives genuine progress.

But everything comes with a cost: Boston is incredibly competitive, causing nearby metros and rural areas - struggling to stay relevant - to lose patients, clinicians, and resources to Boston. Health systems in other MA cities like Worcester and Springfield leak revenue. Cities in other states like Manchester, NH and Providence, RI watch their best doctors migrate east. Even parts of Maine lose patients and specialists to Boston's pull.

This is standard market behavior; resources flow toward jobs and money. It’s just the dynamics of successful enterprises outcompeting weaker ones - except for hospitals, doctors, and scientists. Boston is worth studying for the clear view of healthcare market forces.

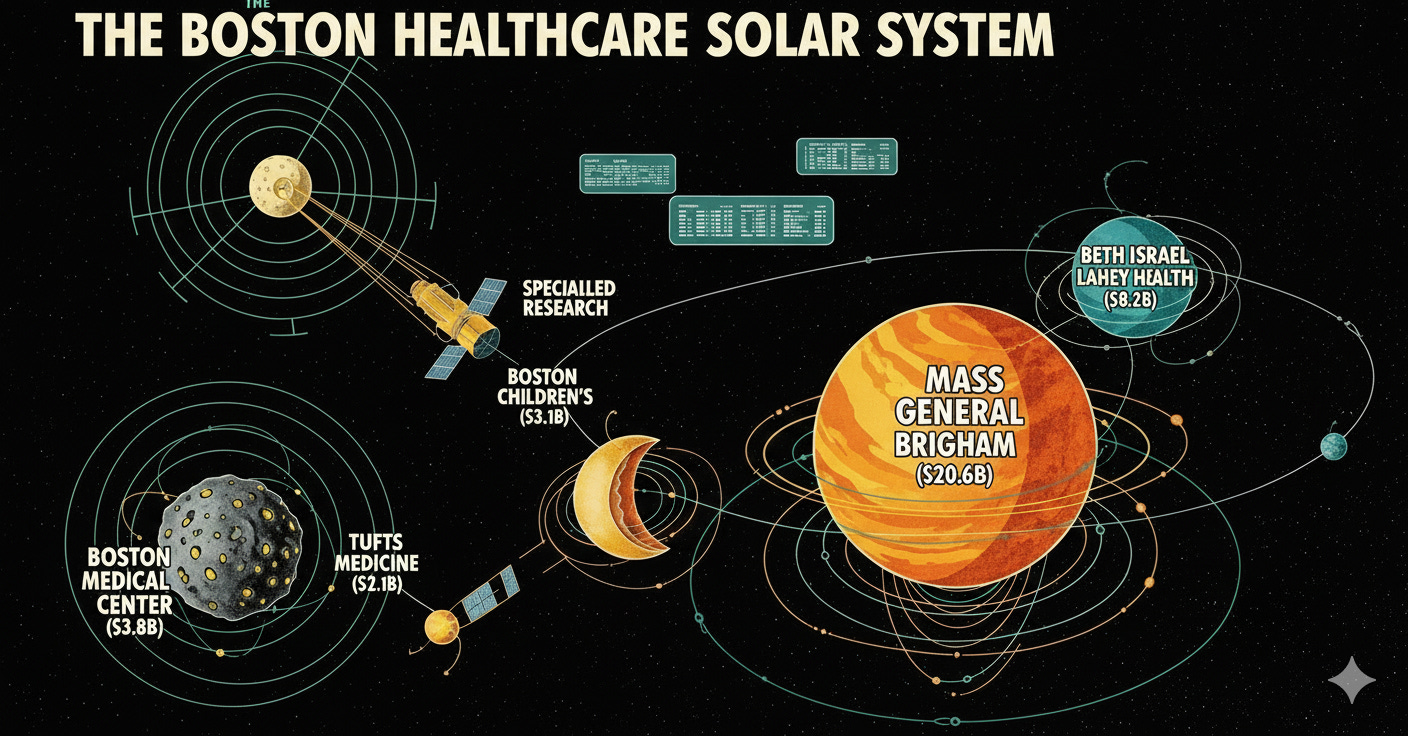

The Planetary Objects

Mass General Brigham ($20.6B net revenue, 4.8% operating margin) - 16 hospitals

If you've met anyone from Harvard, they never forget to mention their university - like the Harvard-affiliated Mass General Brigham. When Mass General Hospital and Brigham & Women's Hospital merged in 1994 (originally called Partners), they created a healthcare juggernaut that dominates everything in sight. MGB is like the overachieving sibling who got into the Ivy League, became a doctor, married rich, and is now in the elite society. They've got the prestige, research dollars, and political connections.

That dominance is well-earned with amazing contributions to healthcare and humanity - but it comes with envious competitors. Market watchers can probably trace every healthcare strategy in Boston as a direct response to MGB. When they tried to expand into affluent suburbs recently, state regulators had to step in and block them because it would have financially gutted community hospitals. That's the MGB paradox - they're so good at what they do that their success threatens everyone else's survival.

Beth Israel Lahey Health ($8.2B net revenue, 2.1% operating margin) - 14 hospitals

Back in 2018, I started a job at another consulting firm. When I first visited the Boston office, only a few people were busy with the merger forming Beth Israel Lahey Health (BILH). That meant merging Beth Israel Deaconess, Lahey Health, and three other hospitals, creating one of the biggest health systems in the state by March 2019. It was obvious to market-watchers: it was to compete with Partners (rebranded to Mass General Brigham in retaliation in Oct 2019).

Hospital mergers are the astronomical event of the healthcare market - like a binary star forming a larger celestial body, creating gravitational waves rippling through the system.

You can see the aftershocks in 2023: the combined BILH, now operationalized, partners with Dana-Farber Cancer Institute’s inpatient oncology program, landing a blow to MGB - Dana-Farber’s previous partner. The acrimonious rift between DFCI and MGB made it to op-ed pieces in the Boston Globe, showing a competitive Boston healthcare market. MGB counter positions by opening their own oncology center. Suddenly, BILH wasn’t just an alternative - it was a serious counterweight to MGB’s dominance.

Boston Medical Center ($3.8B net revenue, 1.4% operating margin) - safety net hospital system with 3 hospitals

Here’s where we discuss smaller, but arguably more “essential” hospital systems in Boston’s healthcare ecosystem: the safety-net Boston Medical Center (BMC) stands out as a nationally respected institution, serving Boston’s vulnerable patient populations, covering 40% of the state’s Medicaid enrollees. BMC and other community hospitals also absorb most uninsured patients, facing political risk (especially due to the recent OBBBA Medicaid cuts), clinical complexity, and financial precarity from other health systems. In the orbit of the city’s academic giants, safety-nets remind us that world-class care often exists because someone else is subsidizing the margins.

Tufts Medicine ($2.1B net revenue, 0.8% operating margin) - 3 hospitals

The last player I’ll get to is Tufts Medicine - the small fish in a crowded New England pond - lacking the scale to compete. And unless it catches the next wave of M&A, it faces the rising tide of Medicare risk adjustments. It risks being swallowed whole or dashed against the rocks.1

This is what market consolidation looks like in real time - you either get big enough to compete, find a merger partner, or get squeezed out. There's no middle ground.

It’s a fun exercise to look at institutional profiles within a market2 - you quickly notice how every merger, partnership, and expansion responds to Boston’s competitive pressure. The forces they exert ripple through every healthcare market in their orbit.

Most people may not recognize the market dynamics in their cities (I certainly didn’t until recently). It’s different when real estate companies, auto dealers, or retail stores compete. The competitive dynamics in one of the densest healthcare markets in the country create more waves than other industries.

These aren't just hospitals and health systems: they're landlords of commercial real estate, the largest employers of a huge tax-paying base, political players connected to city and state agencies, and often competitors for the same pool of funding. They clash and battle like any other free market, and their forces create aftershocks through the region.

The Outer Orbit

Let's drive west down the Mass Pike3 and reflect on the economic impact of the American healthcare system:

Hover over the circles to learn more about each health system

I've lived in Worcester for over a decade, feeling Boston's pull. In 2022, when MGB tried to expand to nearby Westborough - the public health commission, community advocates, and local committees fought back. Why wouldn't a local community want the largesse of a top-tier health system nearby? Well, the other local hospitals who have a history of meeting community needs.

Central Mass has many hospitals, with UMass Memorial Health ($2.9B, 1.9% margin) as the largest outside Boston and the state's only other academic medical center. It occupies a crucial but underappreciated role: sophisticated enough for complex cases, big enough for contract leverage, but ultimately in a smaller pond, constrained by economics in ways Boston's centers aren't.

The patient population is more diverse - serving more rural patients and those with lower socioeconomic status than Boston’s academic medical centers. UMMH generally offers lower-cost care than Boston. Yet, people in Worcester County who choose outmigration to Boston hospitals for specialty referrals, faster appointments, or the prestige of Mass General. That results in tens of millions in losses in commercial insurance payments, Medicare dollars, and procedure revenues flowing east.

The talent drain follows the money - you’re a smart young doctor finishing residency at UMass Chan Medical School (UMMH’s teaching hospital). You can stay in Worcester with modest salaries and its opioid-riddled patient base, or move to Boston where Mass General offers a 50% pay bump, cutting-edge research, and maybe equity in a biotech startup. Such decisions relegate UMass Chan as the farm team that pays to develop talent for the major leagues in Boston.

My hometown Springfield has it even rougher. I was born at the Wesson Women’s Unit at Baystate Health ($2.4B revenue, 0.6% margin), and it pains me to see it lose over $300 million in operating losses since 2022 - forcing three rounds of layoffs and the failed sale of their integrated health plan just to stay afloat.

Baystate Health serves a population with poverty and violent crime rates double the rest of the state, with a fraction of the resources per patient of Boston's academic centers. When a complex case needs specialized care, the patient gets helicoptered to Boston. Springfield pays for emergency stabilization and transport; Boston gets the profitable procedure revenue.

It's the overachieving sibling dynamic on a regional scale. Boston gets all the attention, resources, and opportunities while Worcester and Springfield are relegated to "the other kids" status. State funding, federal research dollars, and private investment flow toward Boston's accomplishments while the rest of Massachusetts makes do with what's left.

The Collapse

Hospitals shouldn’t shut down. It feels like a moral, not an economic, failure. Healthcare system competition and extraction isn’t hypothetical. In 2024, Steward Health Care - once a $6 billion system and Massachusetts’ third-largest - collapsed. The headlines covered the (deserved) story of the greedy private equity’s yacht, but overshadowed how Steward’s community hospitals needed investment to survive in Boston’s hypercompetitive market.

You can drive past the shuttered Carney Hospital in Dorchester, and in its place is a healthcare desert. Carney served a population that was 75% Medicaid and uninsured - the patients that MGB and BILH don't fight over. But even serving this essential safety-net role, Carney couldn't generate the returns that private equity demanded while competing in Boston's orbit.

Running community hospitals with private equity debt loads was a losing battle in a market where academic medical centers have advantages. MGB and BILH duke it out for complex, well-insured patients and research dollars, while Steward gets stuck with high-risk, low-margin cases that academic centers prefer to transfer out.

When Carney closed, those 30,000 annual emergency visits scattered to already-strained Boston emergency departments. The ripple effects hit everywhere - UMass Memorial absorbed more complex transfers, Baystate in Springfield faced tougher physician recruitment as the collapse spooked potential hires about non-academic systems.

Boston's competitive healthcare market isn't just tough - it's becoming existentially brutal for anyone without academic medical center advantages. The same forces that make MGB world-class can crush a $6 billion system.

Physics of the Healthcare Economy

Boston shaped American history. When Paul Revere hopped off his horse on the midnight ride, he became America’s first public health officer. What happens in Boston’s healthcare market plays out in every major American city and state.

Massachusetts is not unique in its market dynamics. New York concentrates everything in Manhattan while upstate struggles. Chicago attracts Midwest talent. Houston drains East Texas. Every major medical hub draws in healthcare resources while suffocating surrounding regions.

There’s nothing unusual about resources collecting around a center - except healthcare is different from every industry. When your local hardware store closes because Home Depot is nearby stealing their business - it sucks, but you just have to go further to get your nails at a cheaper price.

Except in healthcare, costs don’t get cheaper because the larger health system has more negotiating power over the insurance plans. Resource consolidation drowns out competition, and prices actually go up.

Market concentration has life-and-death consequences. When your community hospital loses its cardiac unit because all the cardiologists migrated to the downtown academic medical center, people die waiting for ambulances to make longer trips.

Larger, dominant systems gain more power, leading to innovation and medical breakthroughs - but at a cost to the overall market. Struggling small and mid-sized systems slowly wither away, and large systems weather the storms. It reflects our economy, but in a healthcare system not meant to be financially optimized.

Boston does this more efficiently than most places. We've convinced ourselves it's the only way excellence is possible.

Breaking Orbit

The slow drain of healthcare to dominant metros isn't inevitable - smaller regional health systems have fought this for decades. You could argue for progressive state-level tax policy to redistribute resources, but there are also long-term strategies that lean into homefield advantage.

A friend at Baystate mentioned they'd partnered with UMass Chan Med School partly because their researchers kept leaving for Boston - not just for better pay, but because publishing papers with a Harvard affiliation opens doors that Baystate letterhead won't. It's about keeping talent and the institutional credibility it brings.

The oncology arms race tells this story perfectly. While MGB and BILH vie for cancer prestige in Boston, UMass Memorial built their own Dana-Farber partnership and comprehensive cancer center. Baystate did the same. The marketing is aggressive - running radio ads to stay local for advanced care in Worcester. Every regional system knows that once patients go to Boston for specialized care, they rarely come back for routine stuff. If you handle their cancer treatment locally, you keep their primary care, family's care, and referrals - the whole patient ecosystem.

UMass Memorial's hospital-at-home program works the same way. Patients who would have driven to Boston for complex care are staying in Worcester because they can get the same monitoring and support in their own beds. It's clever market positioning under the guise of patient-centered care.

These approaches sidestep traditional competition. Instead of trying to out-recruit Mass General for cardiac surgeons, they're making geography and convenience the competitive advantage instead of prestige and research funding. When patients can get high-quality care close to home, Boston's gravitational pull doesn't seem so inevitable.

Whether these partnerships can generate enough revenue to offset what these systems lose to Boston remains to be seen. But there's something hopeful about watching regional systems stop playing the big city game and start playing their own.

The Machine We Built

Living an hour west of Boston, you get used to being the little sibling. The one who didn't get into Harvard, didn't make it to the big leagues, didn't measure up to the golden child. Worcester tries hard - we've got decent restaurants now, a minor league baseball team, and a new cancer center partnership with Dana-Farber. But we know who the favorite is.

Boston earned its reputation - the medical breakthroughs are real, the innovation genuine, and the talent undeniable. Take the Longwood Medical Area station off the Green Line and see some of the best healthcare humanity has ever created. The problem isn't Boston's excellence - it's that we've built a system where excellence can only happen in a few special places.

Have we convinced ourselves that healthcare is like any other economic industry? Every research dollar to Harvard Med instead of UMass Chan, every specialist taking the higher-paying Boston job, every patient driving past local care for that prestigious zip code - these are rational choices. They're features of an economic system we designed to reward winner-takes-all competition.

It's the most sophisticated medical extraction machine ever built, and we call it American healthcare.

OK, too many water puns. Something something Charles River.

This is not an exhaustive look. I didn’t even reference Cambridge Health Alliance (another safety-net), or the non-affiliated hospitals, or the VA Hospital in Jamaica Plains (veteran’s healthcare is a whole other beast).

And I purposely omitted a paragraph about Boston Children’s Hospital for a future essay about children’s hospitals and Medicaid cuts.

Again, not exhaustive look. It happens in all directions. Apologies to the cities and rural areas I didn’t cover - your stories are valuable too.

I grew up in Bedford, and my mom is from Springfield! This all rings true to our experience. There is a fantastic former CEO out of Springfield/Ludlow, though, that has been pivotal in changing rural healthcare in MA. If you want an intro, shoot me a DM!

I work at the MGH and have done so for almost 30 years. The healthcare economics are clear. When you are everything to everyone all the time, you become a mile wide and an inch deep. Except that we are deeper in some areas than others. Quality exists all over and quality surgeons for sure, are outside this system. The problem is the gravitational pull to a giant system with marketing that doesn't always jive with outcomes. The real value is the patient outcome. The cost is only part of the equation. I'd make the point that patients now can search for value, and it is not always the largest medical center in the major metropolitan area.